What are CBDCs? A beginner's guide to central bank digital currencies

Is a CBDC a cryptocurrency?

A central bank digital currency or CBDC is a virtual currency backed and issued by a central bank. As cryptocurrencies and stablecoins have grown in popularity, central banks around the world have realized that they must provide an alternative to physical money or risk missing out on the future of money.

Thousands of digital currencies, often known as cryptocurrencies, have already been created. Cryptocurrencies may be centralized, but the government doesn't issue them—consider the Diem project, which has been started by Facebook. However, Bitcoin and its competitors are examples of decentralized cryptocurrencies.

Cryptocurrencies are based on distributed ledger technology (DLT), which means that a transaction’s accuracy is being constantly validated by devices throughout the world rather than by a single central hub.

CBDC is managed on a digital ledger (which may or may not be a blockchain), speeding up and securing payments between banks, institutions and individuals.

Digital currencies issued by central banks are currently one of the most revolutionary innovations in the global financial ecosystem. In the financial world, there have been a lot of questions about the Crypto vs. CBDC discussion. Let's look at various concepts surrounding CBDCs and a comparison between cryptocurrencies and central bank digital currencies.

What is the point of CBDCs?

Cryptocurrencies have been heralded because of their ability to bring in a new era of global financial inclusivity and simplified financial services infrastructure. However, their prominence stems from their capacity as a store of value rather than a medium of exchange. This chasm is gradually closing, with both monetary authorities and commercial entities issuing stabilized cryptocurrencies and CBDCs as viable mainstream payment options.

However, the core concept of a digital currency (replacing the need for paper notes and coins with computer-based money-like assets) has been around for more than a quarter-century. Central agencies were the first to issue digital currencies, such as DigiCash in 1989 and e-gold in 1996.

Nonetheless, Bitcoin's introduction in 2009 changed this model considerably in two ways: It established a decentralized (blockchain-based) ledger for transaction execution and record-keeping, and it created a (now extensively traded) currency independent of any sovereign monetary authority.

The growing significance of digital money during the COVID-19 pandemic, the shift to digital payments, ambitions to employ foreign CBDCs in cross-border transfers and concerns about financial exclusion are all bringing CBDCs into sharper attention.

As a result, the competition to deliver the first genuine version of digital money is heating up among major central banks worldwide. For instance, China is experimenting with a digital Renminbi that allows users to make payments using their mobile phones.

Similarly, as part of the five-year plan, Europe announced the creation of a digital euro. The pandemic hastened the transition to contactless transactions, emphasizing the significance of everyone having access to secure, quick and low-cost payments.

The Federal Reserve is also speeding up its research and public engagement on central bank digital currencies in light of technology platforms integrating digital private money into the United States payments system and foreign authorities studying the possibilities for CBDCs in cross-border payments.

CBDCs appear to be more than just a digital-native replica of traditional notes and coins, according to several public statements. Some governments see CBDCs as programmable money—vehicles for monetary and social policy that might limit their use to fundamental necessities, specific areas or defined periods—in addition to solving the challenge of more comprehensive financial inclusion.

CBDC can take many forms, each having various implications for payment systems, monetary policy transmission and the financial system's structure and stability.

Core features of CBDCs

A CBDC should have instrument, system and institutional characteristics.

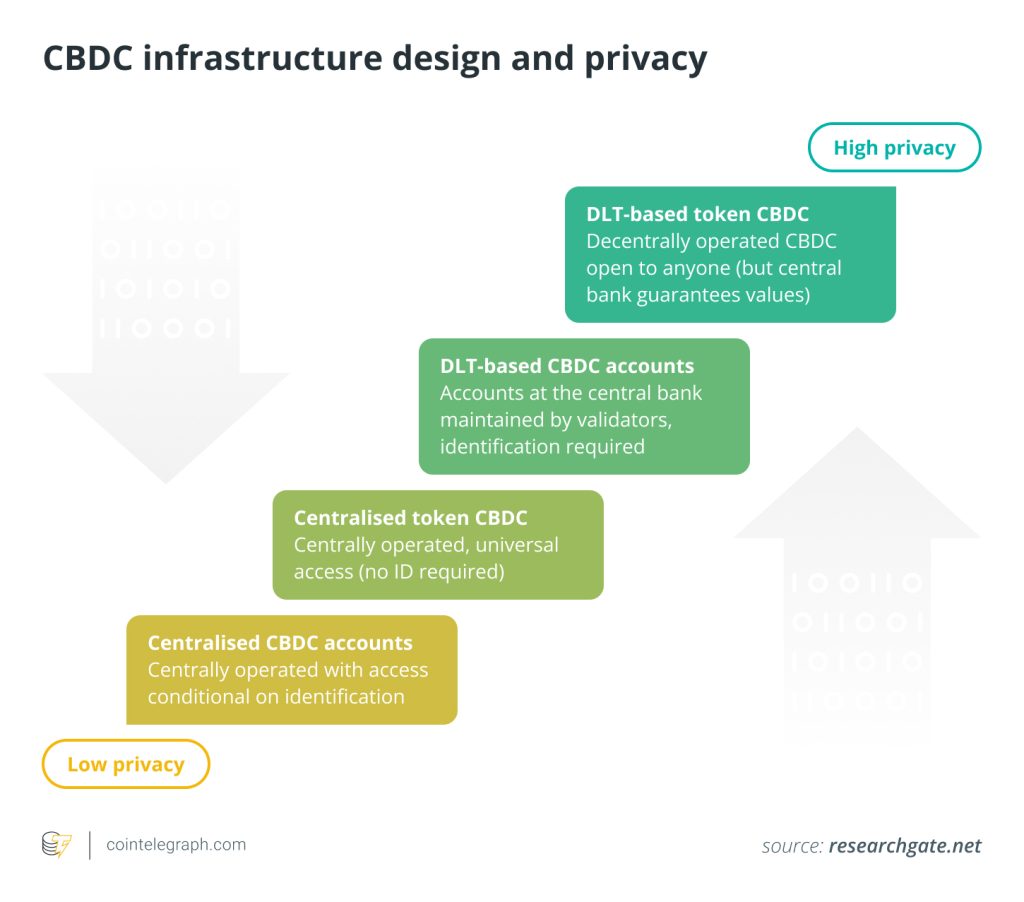

The money flower

Money flower refers to the taxonomy of money in the form of a Venn diagram.

It concentrates on the interactions of four primary components:

-

Issuer (central bank)

-

Form (digital or physical)

-

Accessibility (general or restricted)

-

Technology (token or account-based)

Money is usually based on one of two technologies: stored-value tokens or accounts. Cash and many digital currencies are based on tokens, whereas reserve account balances and most types of commercial bank money are based on accounts.

The type of verification required when exchanging token versus account-based money is a crucial differentiator. The capacity of the payee to check the legitimacy of the payment object is vital for token-based money (or payment systems). On the contrary, account money systems rely heavily on authenticating the account holder's identification.

Digital central bank money lies at the center of the money flower. CBDCs are classified into three types according to the taxonomy (the dark grey shaded area). Token-based and account-based forms are both available.

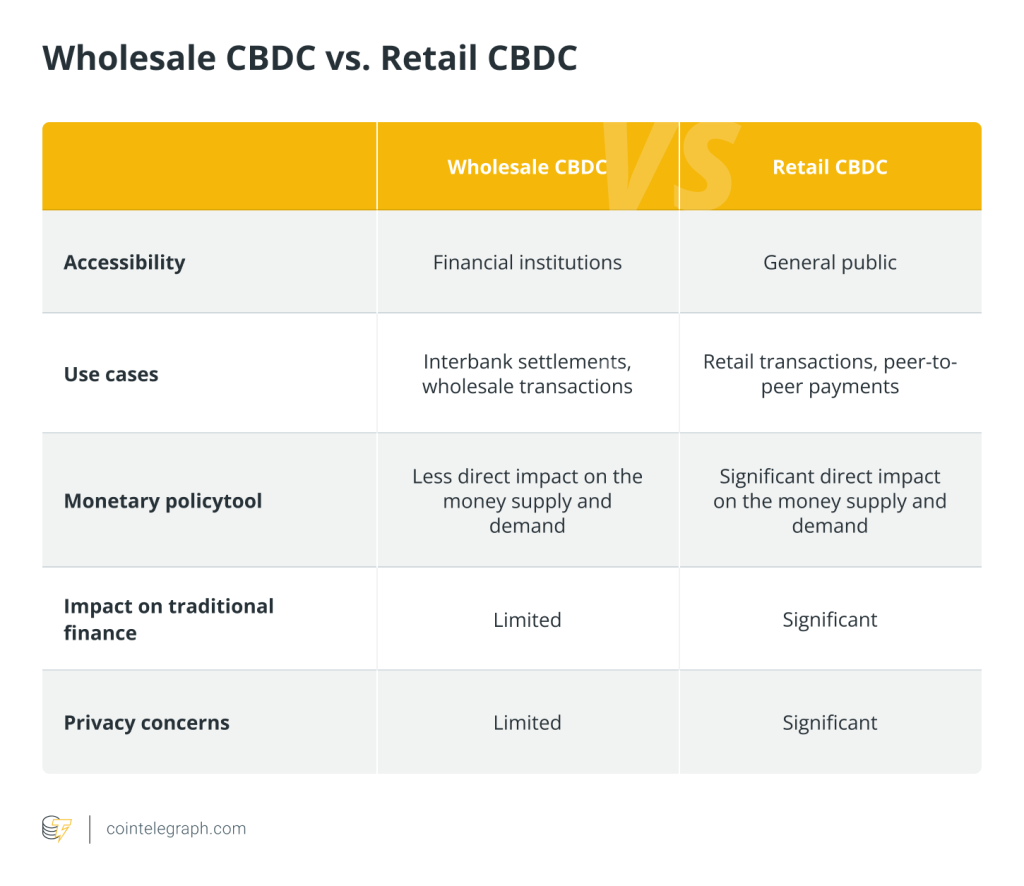

The two token-based variants differ regarding who has access, determined by the CBDC's future use. One is a commonly used payment instrument primarily intended for retail transactions but can also be used for other purposes.

The other is a digital settlement token with restricted access for wholesale payment and settlement activities. They are referred to as general-purpose tokens and wholesale only tokens, as explained in the sections below.

Types of CBDCs

The development of a general-purpose or wholesale only CBDC could help payment, clearing and settlement systems in a number of ways.

General-purpose CBDCs

The term “general-purpose CBDC” refers to a CBDC that will be distributed to the general population. Anonymity, traceability, availability 24 hours a day, 365 days a year, and the feasibility of an interest rate application are all elements of retail CBDC based on DLT.

This idea is gaining traction among central banks in emerging markets, owing to a desire to lead in the fast-growing fintech industry, promote financial inclusion by hastening the transition to a paperless society, and cut currency printing and handling costs.

Wholesale only CBDCs

A wholesale CBDC is for banks that keep reserve deposits with a central bank. It could be used to increase the efficiency of payments and securities settlements and reduce counterparty credit and liquidity risks.

With a restricted-access digital token, a value-based wholesale CBDC would replace or supplement central bank reserves. A token would be a bearer asset, meaning that the sender would transfer value directly to the receiver without intermediaries throughout the transaction.

This would be a significant departure from the current arrangement, in which the central bank debits and credits accounts without actually moving money. Because of its potential to improve existing wholesale financial systems faster, cheaper and safer, the wholesale CBDC is the most favored concept among central banks.

So, in the preceding discussion, we addressed the various sorts of Central Bank Digital Currencies (CBDC). The infographics below will explain the distinction between retail and wholesale CBDCs.

Which countries have a CBDC?

Central bank digital currencies were mainly a theoretical exercise before COVID-19. However, with the need to disperse enormous monetary and fiscal stimulus over the world, as well as the rise of cryptocurrencies, central banks swiftly realized that they can't afford to miss out on the evolution of money.

According to the Atlantic Council, 81 countries (representing more than 90% of global GDP) considered forming a CBDC. Only 35 countries were exploring a CBDC in May 2020.

China is ahead of the game, enabling foreign visitors to use digital Yuan to provide passport information to the People's Bank of China for the upcoming Winter Olympics. The United States Federal Reserve is the furthest behind the other large central banks, the European Central Bank, the Bank of Japan, and the Bank of England.

A digital currency has now been wholly launched in five nations. The first CBDC to become widely available was the Bahamian Sand Dollar. Fourteen nations, including large economies like Sweden and South Korea, are currently testing (i.e., at a pilot stage) CBDCs for a full launch.

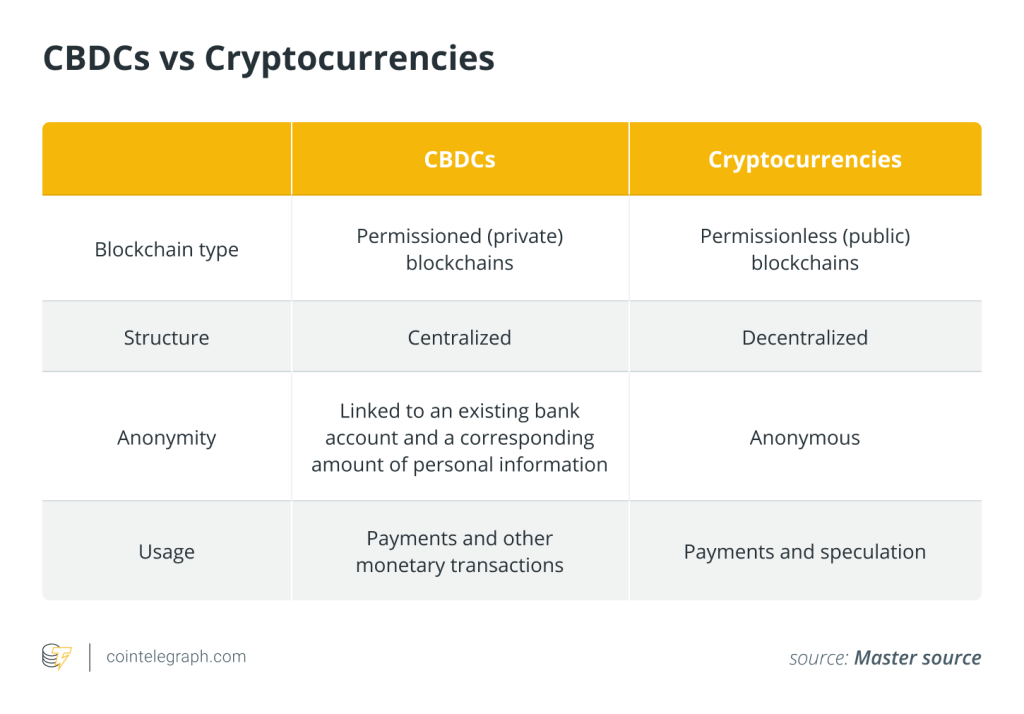

CBDC vs Cryptocurrency

Digital currencies issued by central banks are commonly mistaken for other types of cryptocurrency. As stated previously, central bank digital currencies have central banks at the heart of every transaction. However, cryptocurrencies, such as Bitcoin, are digital tokens created using cryptographic methods by a distributed network or blockchain.

Cryptocurrencies employ permissionless (public) blockchains, whereas CBDCs use permissioned (private) blockchains. Anyone can join and participate in the blockchain network's essential operations in a public blockchain. The ongoing operations on the public blockchain network can be read, written and audited by anybody, which helps a public blockchain preserve its self-governed nature. A private blockchain, on the other hand, is a distributed ledger that functions as a closed, secure database based on cryptography concepts and is not decentralized.

The restrictions on CBDC networks are set by a central bank. The authority is assigned to the user base on crypto networks, which makes choices by achieving a consensus.

Therefore, while cryptocurrencies are decentralized, CBDCs are centralized. Moreover, cryptocurrencies provide anonymity; CBDCs allow central banks to see who owns what. CBDCs are more likely to run on distinct technological platforms than cryptocurrencies, which are often established utilizing blockchain.

CBDCs are also not stablecoins, which are currencies that are pegged to a fiat currency like the U.S. dollar. A CBDC would not be pegged to a fiat currency; instead, it would be the fiat currency itself. For instance, a CBDC dollar bill would be identical to a dollar bill.

CBDCs can only be used for payment, and any stockpiling or investing is outright prohibited. Nonetheless, cryptocurrencies can be used for both financial transactions and speculation purposes.

In comparison to cryptocurrencies, a CBDC would be less concerned about data and privacy. The crypto sector is unquestionably autonomous with a peer-to-peer paradigm, whereas certain restrictions bind central banks.

Users can choose how much and what kind of data they wish to disclose because cryptocurrencies are peer-to-peer. On the contrary, CBDC transactions will automatically send vast amounts of data to tax and regulatory agencies.

How are CBDCs different from Bitcoin?

Bitcoin may have been the first crypto to gain widespread acceptance, and it certainly dominates blockchain and crypto discussions, but it is just one of the thousands of crypto assets available.

The attraction, utility and principles of Bitcoin have not been weakened or lessened by the advent of different crypto variants. Instead, the growth of stablecoins, CBDCs and other blockchain and crypto-related applications has improved the ecosystem's overall health.

The Bitcoin ecosystem offers a glimpse of an alternative financial system in which transaction terms are not dictated by onerous regulation. Bitcoin, which was founded in 2009, is one of the world's most popular cryptocurrencies. Bitcoin doesn’t represent tangible coins that change hands. Transactions are instead traded and recorded in a public, encrypted ledger that anyone can access. All transactions can be validated via the mining process. Banks or governments do not back Bitcoin.

CBDCs are supposed to be used as a substitute for fiat currencies. The idea is to provide consumers with the ease and security of digital as well as the traditional banking system's regulated, reserve-backed circulation. They're made to serve as a store of value, a unit of account and a medium of exchange in everyday transactions.

CBDCs, like fiat currency, will be backed by the issuing government's complete confidence. For their operations, central banks or monetary authorities will be fully responsible.

Pros and cons of central bank digital currencies

Pros

CBDCs make monetary policy and government functions easier to implement. They use wholesale CBDCs to automate the process between banks and retail or general-purpose CBDCs to directly connect customers and central banks. Other government services, such as the distribution of benefits and the calculation and collection of taxes, can benefit from these digital currencies by reducing work and processes.

Money is disbursed through intermediaries, which introduces a third-party risk into the transaction. What happens if the bank's cash deposits run out? What if a bank run occurs due to a rumor or an external occurrence such as a financial crisis? Such events can disturb a monetary system's delicate balance. A CBDC eliminates the danger of a third party because the central bank is responsible for any remaining risk in the system.

In a CBDC system, privacy characteristics can be calibrated. A value-based retail CBDC works like currency and protects personal information by keeping transactions anonymous. Account-based access to CBDCs, on the other hand, works like a conventional bank account and can include privacy protections.

CBDCs can deter illegal activities because they are stored digitally and do not require serial numbers to be tracked. A central bank can easily trace money using cryptography and a public ledger throughout its jurisdiction, prohibiting criminal activities and illegal CBDC transactions.

The expense of creating the banking infrastructure needed to provide them with access to the financial system is one of the barriers to financial inclusion for vast segments of the unbanked population, particularly in developing nations. CBDCs can create a direct link between customers and central banks, obviating the need for costly infrastructure.

Cons

CBDCs aren't always the answer to the problem of centralization. The authority to conduct transactions is still delegated to and vested in a central authority (i.e., the central bank). As a result, it still influences data and transaction levers between citizens and banks.

Because the administrator is in charge of collecting and disseminating digital identifications, users would have to give up some privacy. Every transaction would be visible to the service provider. This could lead to privacy concerns similar to those experienced by IT giants and internet service providers (ISPs). Criminals could, for example, hack and misuse information, or central banks could prohibit citizen-to-citizen transactions.

CBDCs can help with cross-border and cross-currency payments that aren't constrained by work hours or holidays in various time zones. Different legal and regulatory frameworks, on the other hand, create a considerable barrier to cross-border payments. It would be challenging to bring these frameworks together.

CBDCs may have unintended effects on foreign exchange markets. For example, China's CBDC is meant to threaten the dollar's dominance: If the digital yuan becomes the primary payment tool in China, global companies will be forced to use it to do business, potentially affecting the dollar's role.

The road ahead

The CBDCs would disrupt the current fractional reserve system, allowing commercial banks to create money by lending out more than they have in liquid deposits. Deposits are required by banks for them to make loans and investment decisions.

Traditional banks would have to become “loanable funds intermediaries,” borrowing long-term funds to finance long-term loans like mortgages if all private bank deposits were shifted into CBDCs.

A narrow banking system, mainly overseen by the central bank, would replace the fractional-reserve banking system. That would amount to a financial revolution — one with numerous advantages. Central banks would be considerably better equipped to prevent bank runs and monitor private banks' risky credit/lending choices.

A well-designed CBDC will be a secure and impartial payment and settlement asset, acting as a shared interoperable platform for the new payment ecosystem to organize itself around. It will allow for an integrated open finance architecture that welcomes competition and innovation. It will also maintain democratic control over the currency.

… [Trackback]

[…] Find More on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Here you will find 80053 additional Information on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Information to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Find More Information here on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Here you will find 41990 more Info on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More on on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/beginner/2403/ […]

cinemakick

… [Trackback]

[…] Here you can find 8672 additional Information on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More Information here on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More Information here to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Info on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] There you can find 98329 more Info on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] There you will find 69520 more Info on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More Info here to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Info to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Info to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More Info here on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More Info here to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Here you can find 64548 additional Information to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More Information here to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Information to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More here to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Info to that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Find More Info here on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Find More here on that Topic: x.superex.com/academys/beginner/2403/ […]

… [Trackback]

[…] Read More here on that Topic: x.superex.com/academys/beginner/2403/ […]