Ethereum futures open interest hits 19-month high, yet ETH price weakness intensifies

Ethereum derivatives metrics show increased activity, indicating higher interest but not necessarily a bullish trend.

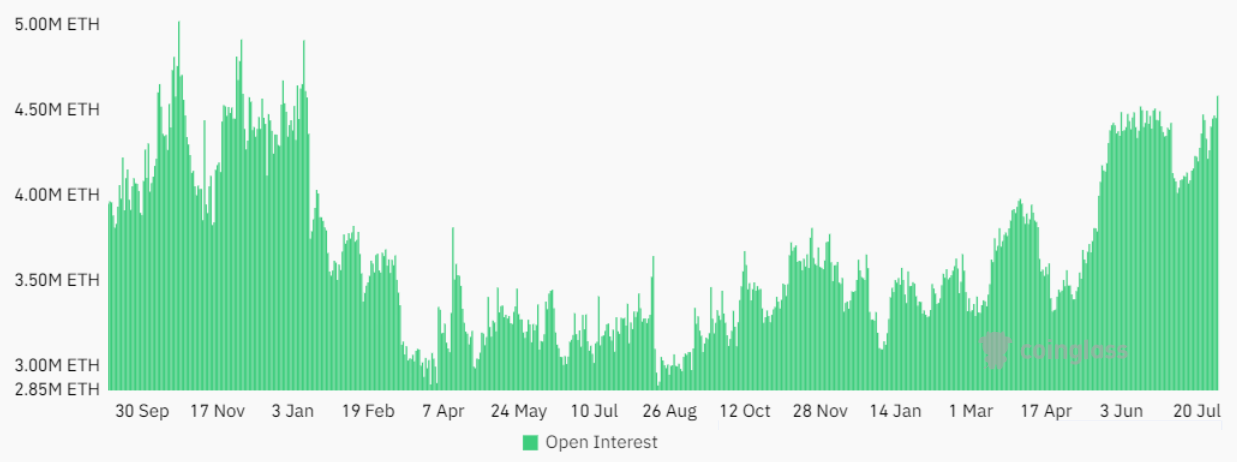

Ether (ETH) experienced a 10% correction between July 31 and Aug. 2, retesting the $3,000 support for the first time since July 8. This movement significantly outpaced the broader cryptocurrency market, which declined by 6.8% during the same period. Despite this, Ether futures open interest rose to its highest level in seven months, leading traders to speculate whether a rally to $3,600 is the next probable move.

Increased interest in Ether futures is not necessarily bullish

The increased activity in ETH futures contracts typically indicates institutional investors’ interest, as open interest measures the demand for leverage. However, buyers (longs) and sellers (shorts) are always matched, so an increase in open interest does not inherently indicate a positive outlook.

Part of Ether’s decline can be attributed to the lack of net inflows into recently launched Ether exchange-traded funds (ETFs) in the United States. Although there were some inflows, particularly into BlackRock’s iShares Ethereum Trust and the Fidelity Ethereum Fund, these were offset by outflows from the Grayscale Ethereum Trust, which has existed since before the ETF conversion.

Ether’s drop below $3,000 triggered $141 million in leveraged long liquidations within 48 hours, further fueling the correction. However, this did not deter other traders from entering the market, regardless of whether they were betting on Ether’s price rising or falling. Consequently, the aggregate open interest in Ether futures increased by 5% over seven days, reaching 4.6 million ETH, the highest level since January 2023.

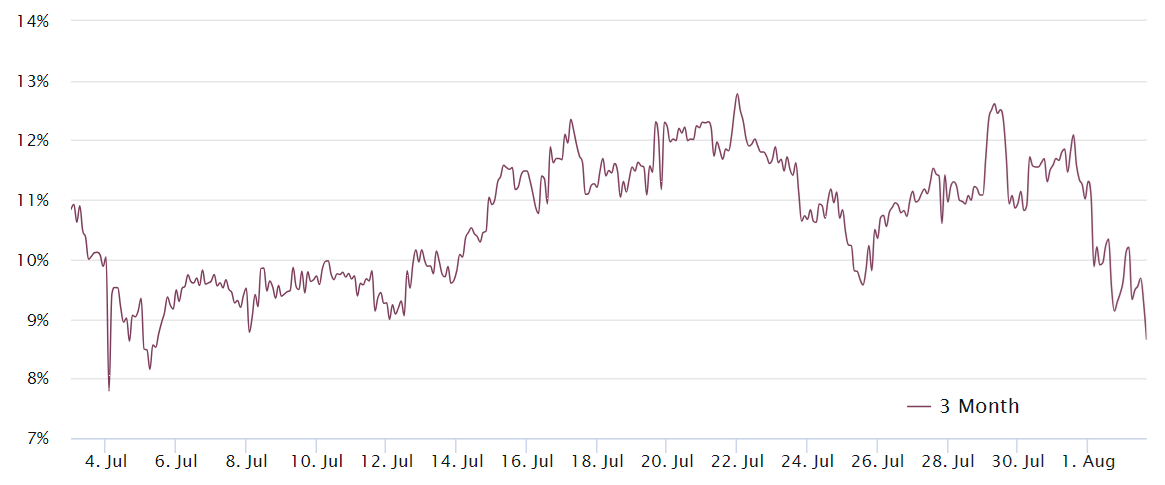

To determine if buyers are demanding more leverage, one should analyze how ETH futures monthly contracts are priced relative to regular spot exchanges. In neutral markets, these derivatives should trade 5% to 10% higher, annualized, to compensate for the longer settlement period. Thus, if traders are becoming bearish, this indicator would likely fall below that threshold.

Ether monthly futures contracts showed modest optimism in the days preceding the spot ETF launch on July 23, with the futures premium reaching 12%. However, subsequent net outflows from spot ETFs and a broader crypto market correction caused the index to drop to 8% on Aug. 2. This level is neutral but not unusual considering the 10% price decline over 24 hours.

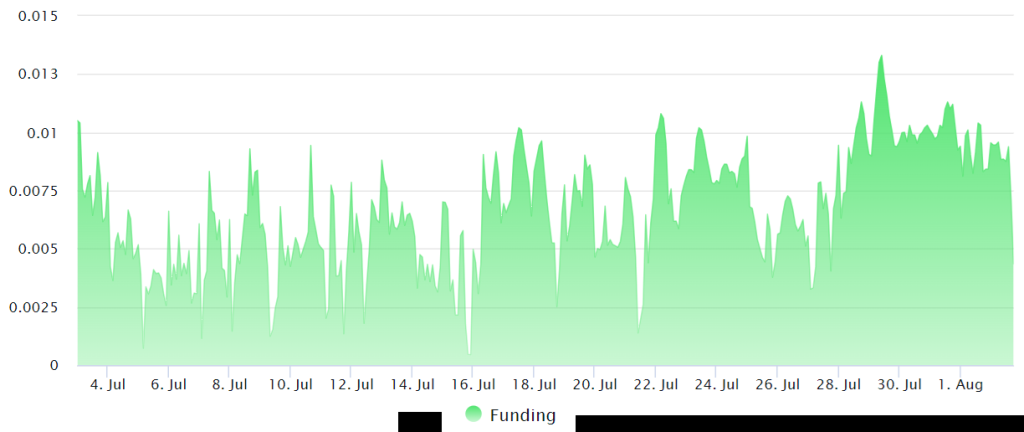

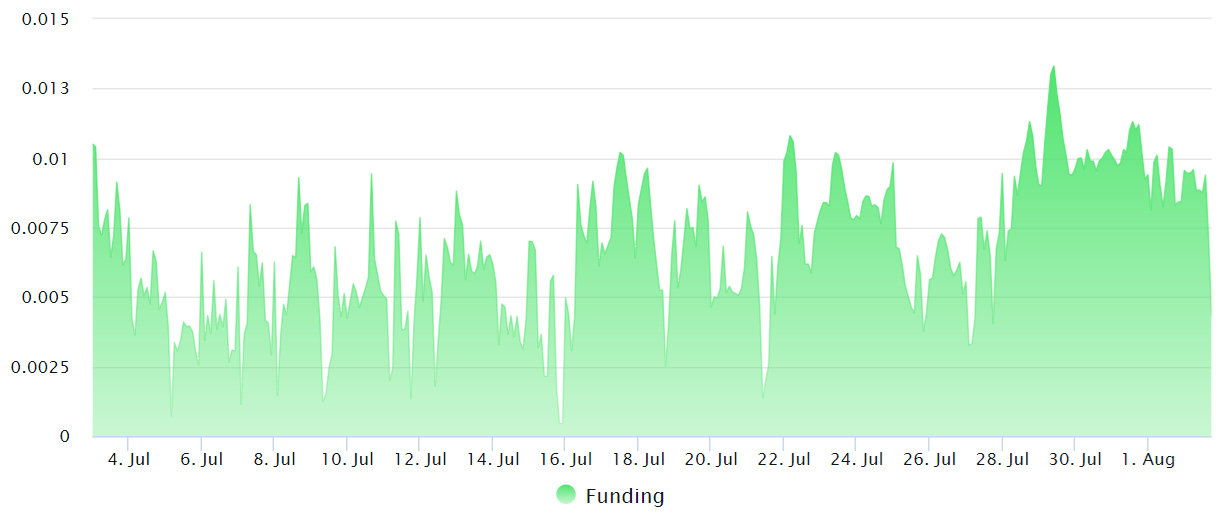

Retail demand for ETH leveraged longs has been stagnant

To assess the leverage demand for retail traders in Ether futures, one should examine the perpetual contract (inverse swap) funding rate. Unlike monthly contracts, these instruments tend to closely follow the spot price due to their shorter settlement times. Typically, exchanges adjust risk every eight hours by charging a fee to the side demanding more leverage, meaning either longs or shorts pay the fee.

In neutral markets, the eight-hour funding rate ranges from zero to 0.016%, equivalent to 1.3% per month. During periods of heightened optimism, this rate can easily exceed 0.025%, or 2.1% per month.

Related: Ethereum’s firm $2,860 support signals path to $4,500 — Deribit

The Ether eight-hour funding rate has been relatively stable at 0.008%, equivalent to 0.7% per month, well within the neutral range. This has been the norm for the past few days, indicating that retail traders were not heavily relying on excessive leverage prior to the unexpected price drop to $3,000.

The primary driver for the increase in Ether futures open interest has most likely been the cash-and-carry trade, a neutral arbitrage strategy. Investors sell futures contracts to capture the premium while simultaneously buying the spot or ETF to hedge their risk. Therefore, according to ETH derivatives metrics, there is currently no indication that traders are anticipating a short-term price pump.

Responses