Celo integrates Chainlink's CCIP interoperability protocol

The Ethereum layer-2 solution is leveraging Chainlink for blockchain interoperability and real-world price data.

On May 29, Ethereum layer-2 network Celo announced the integration of Chainlink’s CCIP protocol for cross-chain interoperability.

Celo’s executive director, Eric Nakagawa, issued a statement following the deployment of CCIP on Celo: “Canonical cross-chain infrastructure can accelerate the long-term growth and adoption of the Celo ecosystem.” Nakagawa added, “As the only interoperability solution achieving level 5 cross-chain security, CCIP provides a great option for developers, founders, and the wider community to consider and adopt.”

Cross-chain interoperability continues to be a core focus of the blockchain industry as real-world asset tokenization is poised to become the next major frontier for growth.

According to Chainlink, the total of all real-world assets accounts for a staggering $874 trillion in value. Even a small portion of that value coming to the blockchain

Unfortunately, these assets are spread out across numerous platforms, industries, and chains, causing efficiency and liquidity issues for investors and speculators who wish to unlock value embedded in traditionally illiquid assets such as real estate and collectibles.

Chainlink’s CCIP protocol

This is where Chainlink’s CCIP protocol comes in. It acts as a sort of ‘layer 0’ protocol for cross-chain communication between public blockchains and even traditional financial architecture.

Related: Arta TechFin, Chainlink expand partnership to tokenize real-world assets

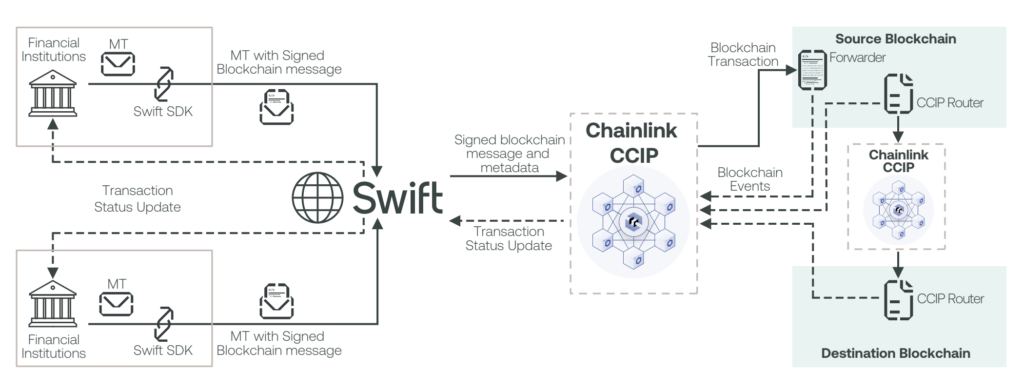

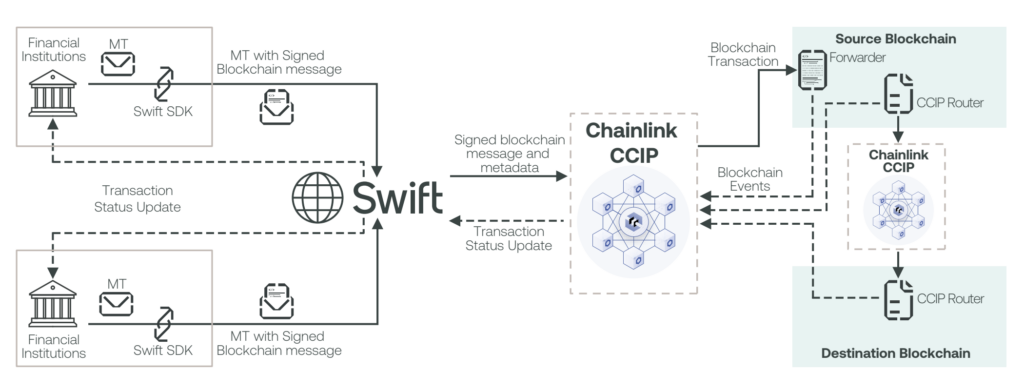

In 2023, Chainlink successfully conducted a pilot test with SWIFT—the international messaging protocol for interbank communication.

The oracle network and interoperability protocol also conducted a similar experimental test with the Depository Trust and Clearing Corporation (DTCC) and several banking partners, including JP Morgan and BNY Mellon, to bring real-world assets on-chain.

Chainlink’s experiments with SWIFT and the DTCC highlight the potential synergies between blockchain, traditional banks, and international business.

Existing problems with cross-border transactions

Currently, cross-border transactions are sluggish, costly, and inefficient, with a bevy of intermediaries inserting themselves within the transaction.

Payment processors, banks, credit card companies, and information processors all join in on the transaction, each taking their own cut in the form of fees and slowing down the transaction.

Additionally, regulatory compliance also bogs down transactions with inefficiencies and costly fees that hinder transaction finality and prevent smaller players from conducting business internationally.

Much of the business world is still operating on outdated technology in the digital age, which is why it often takes days for a traditional bank transaction to post. This also applies to simple, domestic transactions that do not rely on cross-border messaging.

Responses