Starknet-based ZKX protocol shutters, blaming lack of users

The protocol’s founder cited minimal user engagement, tumbling revenues, and “broader exhaustion” in the DeFi sector.

The ZKX Protocol — a social derivatives trading platform built on the Ethereum Layer-2 network Starknet — has shuttered, with its founder saying there is no “economically viable path” forward for the protocol.

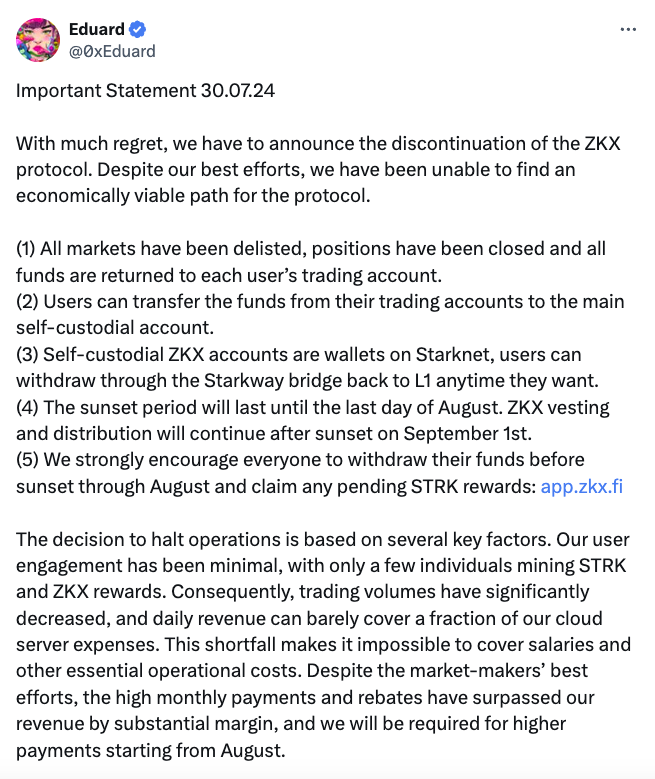

In a July 31 post to X, ZKX founder Eduard Jubany Tur wrote that the protocol’s user engagement had been “minimal,” noting that only a few individuals had been mining the protocol’s rewards program.

He added that trading volumes had “significantly decreased” and the protocol’s daily revenue could only cover a “fraction” of their cloud server expenses.

Tur said ZKX had delisted all markets, closed all positions, and returned all funds to each of its user’s trading accounts. Users will have until the end of August to transfer their funds from their trading wallets to the protocol’s main self-custodial account.

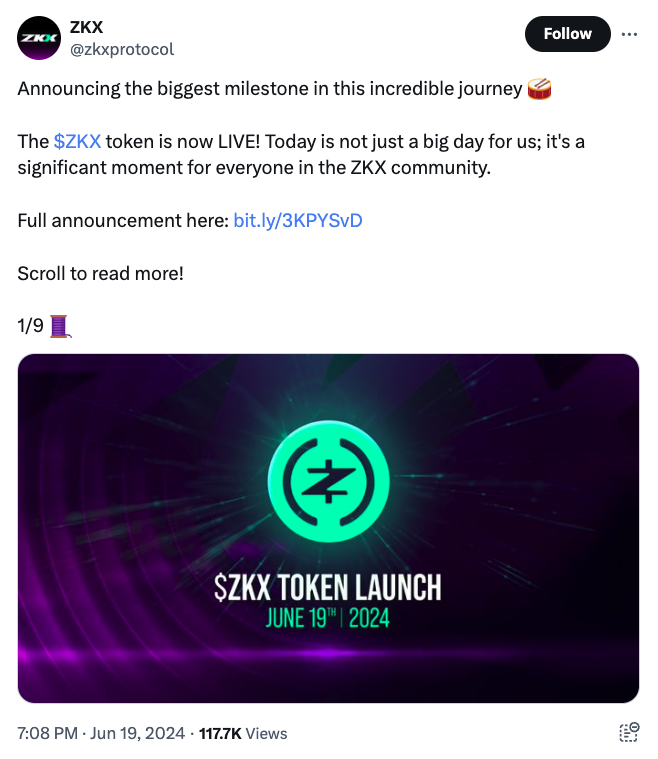

It comes just a month after ZKX protocol raised $7.6 million in funding from a strategic round on June 19, which saw contributions from investors including Flowdesk, GCR, and DeWhales.

Previous investors in the protocol included Hashkey, Amber Group, Crypto.com, and StarkWare.

Tur added there was no way to “sustainably support” the protocol with the current value of its recently launched ZKE token.

Related: Starknet launches $25M token incentive for top projects

“There’s no denying the TGE didn’t meet expectations, and the resulting losses have contributed to our current situation. As major token holders exercise their right to cash out, the token’s value has continued to decline,” he said.

Tur also blamed “broader exhaustion” in the decentralized finance (DeFi) sector.

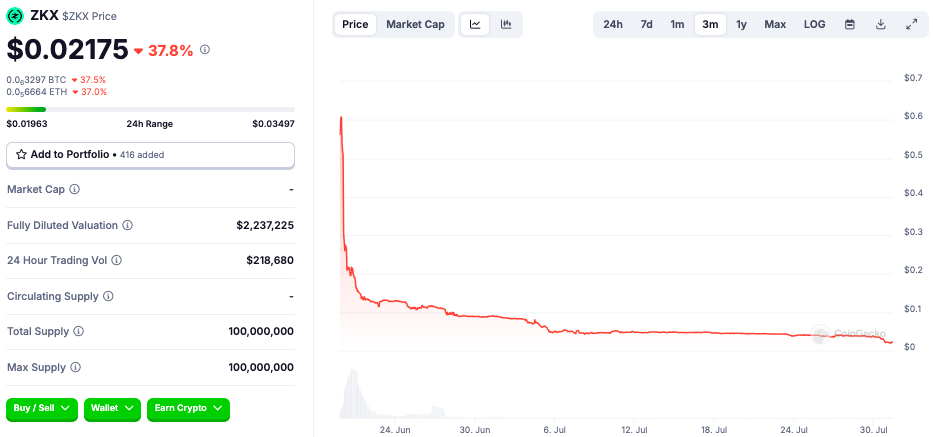

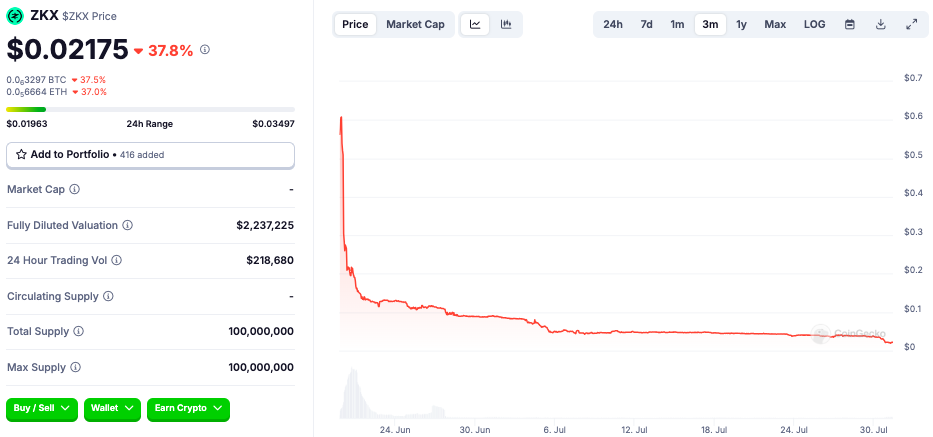

The price of the protocol’s native ZKX token fell 37.8% in the last 24 hours and is currently changing hands for $0.02, per CoinGecko data.

The ZKX token is down 96.4% from its all-time high of $0.62 which it notched a day after its launch on June 20.

Responses