$1.35B in Bitcoin options expire this week — Do BTC bulls or bears have the upper hand?

This week’s Bitcoin options expiry sits at $1.35 billion, but what is the expected impact on BTC price?

Whenever Bitcoin’s (BTC) price action exhibits significant corrections, analysts and traders are quick to search for a reason, often pointing fingers at derivatives markets where bears allegedly exploit futures contract liquidation levels or anticipate increased profits from weekly BTC options expiries.

Such talk has been on the decline recently, thanks to Bitcoin’s range-bound price action, but now that murmurs of a trend reversal have come back, let’s take a look at how whales are positioned using Bitcoin derivatives markets.

Will the May 10$1.35 billion BTC options expiry bring volatility?

The recent failure to maintain prices above $65,000 on May 6 is an example of how some market participants blame the weekly options expiry for the recent downtrend. If this were the case, which can be inferred by BTC derivatives metrics, further downward pressure could be expected ahead of the 8:00 am UTC expiry on May 10.

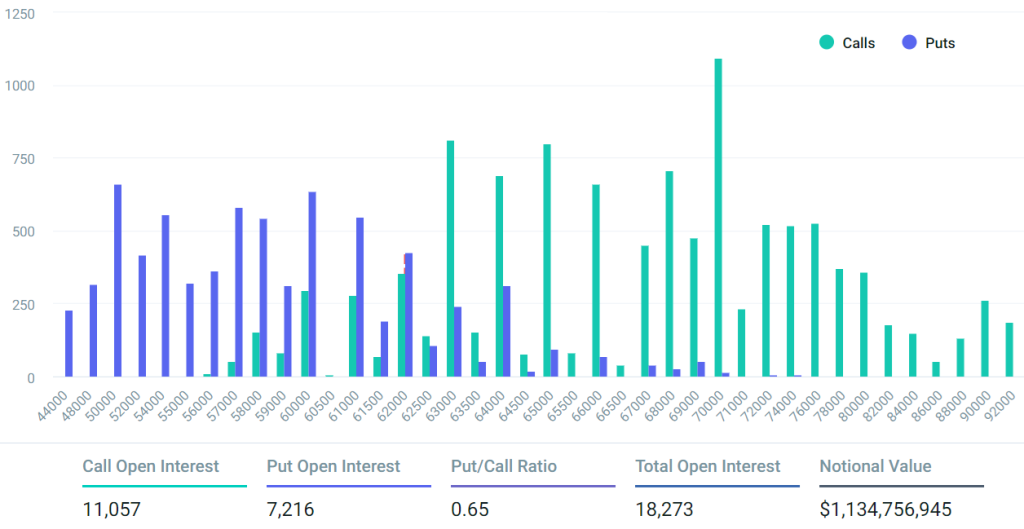

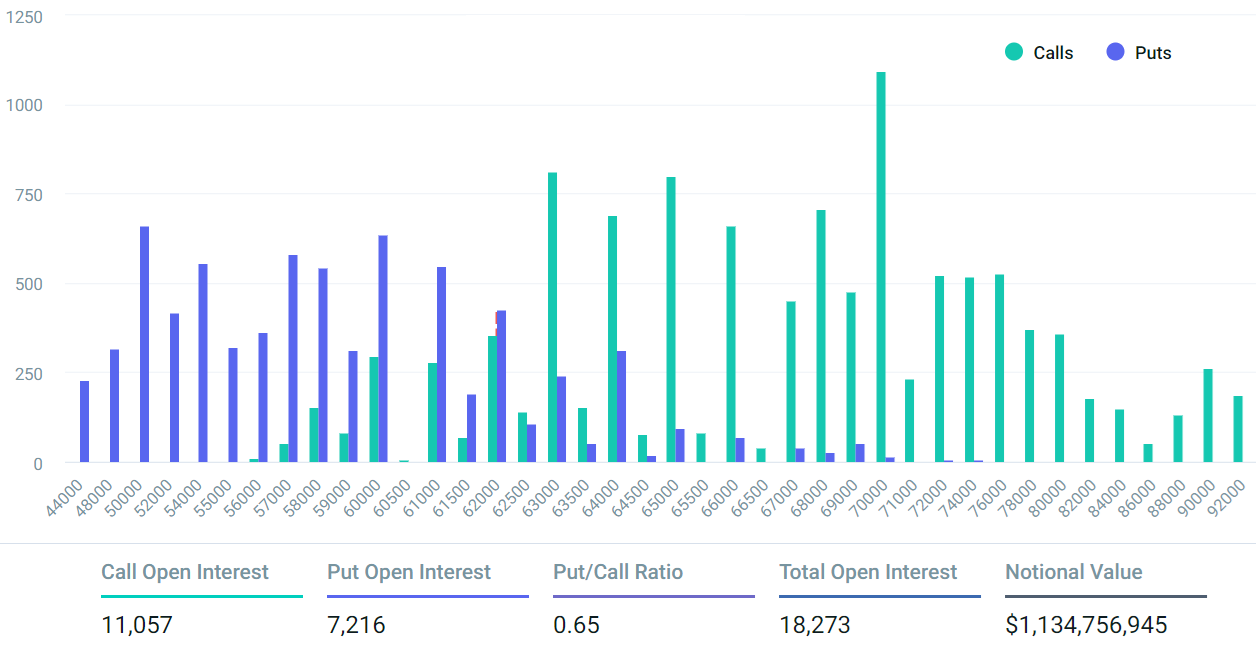

From a top-down perspective, the $1.35 billion options open interest seems substantial enough to justify the effort from Bitcoin bears. However, a more detailed analysis reveals a different scenario. Deribit holds an 84% market share for the May 10 options expiry, so data will primarily be extracted from that exchange. Since the Chicago Mercantile Exchange (CME) only offers monthly contracts, it was excluded from the analysis.

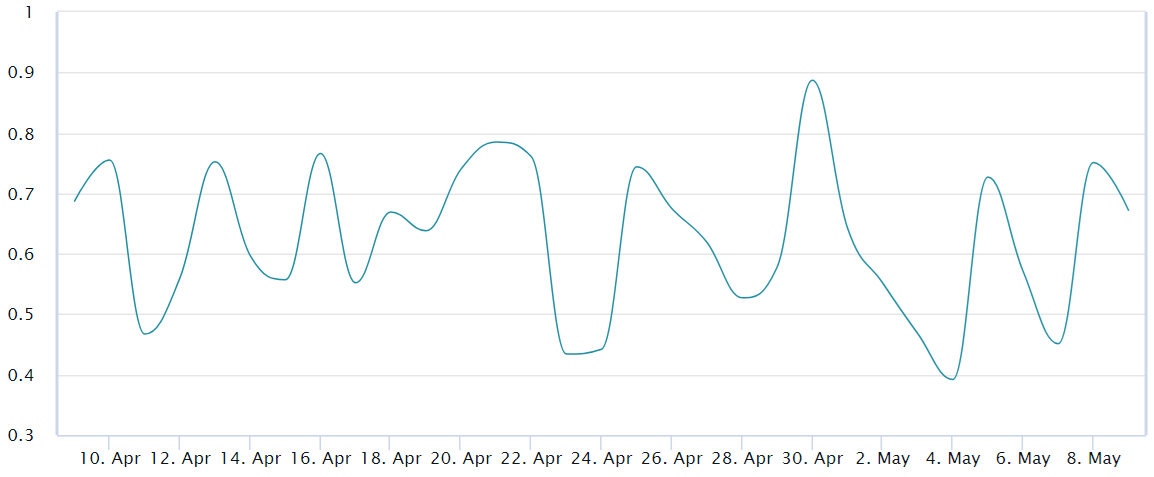

It’s worth noting that call (buy) and put (sell) options are not always matched when stacked against each other, a common feature for such instruments regardless of the underlying asset. Thus, the first relationship to consider is the volume discrepancy between these instruments. Generally, increased demand for puts indicates bearish markets.

Note that the average BTC options put-to-call volume at Deribit stood at 0.60 for the past 10 days, meaning put (sell) instruments had 40% lower volumes compared to call (buy) options, which has been the norm for the past month. In essence, it’s difficult to justify that bears have set some kind of trap or anticipated Bitcoin’s failure to sustain $65,000 on May 6.

Bitcoin bulls cast overly optimistic bets

However, one should not take every call option buyer at face value, especially given that there are less than 13 hours ahead of the actual expiry on May 10. For instance, there is hardly a way to justify a right to buy Bitcoin at $74,000 or even $90,000 in such a short time. Therefore, one should not account for those overly optimistic bets when measuring the open interest.

Even though the put-to-call ratio shows a 35% lower demand for put options, bears are at less risk, as most of the call instruments were placed at $63,000 and higher. In fact, the open interest for call options below this level is $91 million, which means 87% of them will be worthless on May 10. However, if Bitcoin bulls manage to reestablish the $64,000 support, the open interest for call options will surpass the put instruments by $115 million.

Related: Despite Bitcoin price volatility, factors point to BTC’s long-term success

While bears may have avoided significant losses had Bitcoin stayed above $65,000, this doesn’t necessarily mean they will come out ahead in the end. Put options at $61,500 or higher have a total open interest of $104 million, which is just enough to balance the equation. The best-case scenario for bears requires a Bitcoin price below $61,000 to secure a $100 million advantage.

There is no indication that Bitcoin bears placed additional bets using BTC options to profit from a price crash ahead of the May 10 expiry. There was no unusual demand between put and call instruments, and there is no specific price level that greatly benefits bears. Whatever strategies were employed, the result is an apparent balanced impact at $62,000, suggesting no price surprises are expected.

Responses