Virginia proposes $39K yearly fund for crypto and AI commissions

The proposal allocates a yearly general fund of $22,048 and $17,192, respectively, to the two newly formed commissions on artificial intelligence and cryptocurrency in the state of Virginia.

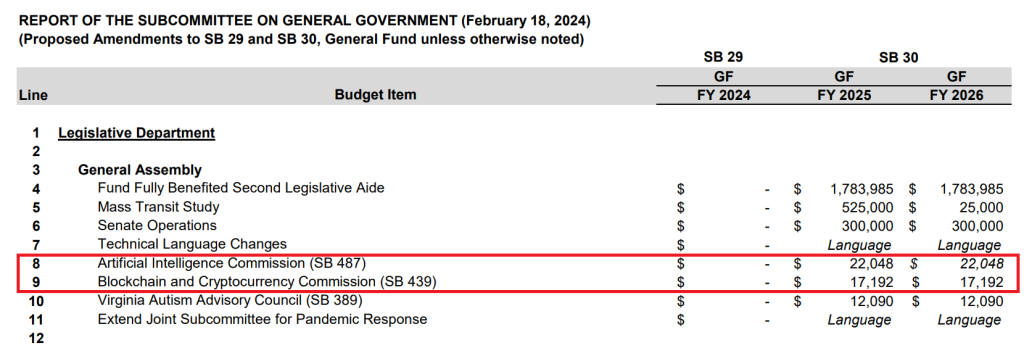

A Virginia senate committee has recommended a yearly combined fund allocation of $39,240 for two newly formed commissions on artificial intelligence (AI) and cryptocurrency.

A Feb. 18 proposal from the Subcommittee on General Government of the Senate Finance and Appropriations Committee allocated over $23.6 million for various legislative departments. Out of the total, the Blockchain and Cryptocurrency Commission, established in January 2024, received a proposed general fund of $17,192 for 2025 and 2026.

The Artificial Intelligence Commission, currently called the Committee on Communications, Technology and Innovation, was allotted $22,048 for the same period.

The Blockchain and Cryptocurrency Commission is tasked with studying and making recommendations for blockchain technology and crypto and fostering expansion within the state. It will comprise 15 members, including seven legislative and eight nonlegislative members, to be appointed “no later than 45 days after the effective date of this act.”

Similarly, the Artificial Intelligence Commission aims to develop and maintain policies that will eventually limit the use of AI to avoid unlawful activities.

The bill to amend the Code of Virginia and establish the blockchain and crypto commission was introduced on Jan. 9. The Senate unanimously passed it on Feb. 1.

Related: US Virginia bill seeks working group to study crypto, blockchain

In addition to establishing fresh legislative commissions around crypto and AI ecosystems, Virginia recently introduced crypto mining legislation that favors individuals and businesses.

Senator Saddam Azlan Salim proposed Senate Bill No. 339 on Jan. 9, which aims to exempt miners from obtaining money transmitter licenses. The bill also prohibits industrial zones from imposing mining-specific ordinances:

“No license under this chapter shall be required of any person engaging in-home digital asset 37 mining, digital asset mining, or digital asset mining business activities, as those terms are defined in § 38 15.2-2288.9.”

While companies offering mining or staking services cannot be classified as a “financial investment” under the bill, they must file a notice to qualify for the exemption.

The legislation proposes that individuals can exclude up to $200 per transaction from their net capital gains for tax purposes. This exclusion applies to gains derived from using digital assets to purchase goods or services. As a result, the bill incentivizes the use of cryptocurrencies for everyday transactions via tax benefits.

Responses