Bitcoin futures open interest hits all-time high — Is it a red flag for BTC price?

Traders’ strong appetite for leverage could be creating the perfect scenario for cascading liquidations.

Bitcoin (BTC) soared above $72,000 for the first time ever on March 11, marking a 9.5% increase over the past week. The rally has seen significant volatility, highlighted by a 4.8% intraday rise to $70,055 on March 8, followed by a 5.9% dip to $65,935.

As a result, Bitcoin bulls are wary of celebrating this new all-time high, particularly due to the surge in leverage demand through BTC futures contracts.

Demand for Bitcoin futures soar, but that’s not necessarily bullish

Analysts have pointed out that the $35.8 billion in Bitcoin futures open interest poses a risk, as traders often over-rely on leveraged positions.

This data confirms investors’ interest, but it cannot be deemed inherently bullish because futures longs (buyers) and sellers (shorts) are matched at all times. This situation creates volatility rather than directional bias.

It is also worth mentioning that the Chicago Mercantile Exchange (CME) presently holds the largest share in Bitcoin futures, surpassing traditional crypto exchanges such as Binance, Bybit, and OKX. However, this was not the case in November 2021 when Bitcoin futures open interest last peaked as BTC traded near $69,000, subsequently experiencing a 31.5% decline in just 30 days.

When this figure is expressed in BTC, the Bitcoin open interest remains 27% below its October 2022 peak. Yet, the current 495,380 BTC in futures open interest is substantial enough to trigger sharp volatility spikes as Bitcoin’s price fluctuates. This was evident on March 4, when a staggering $325 million in leveraged BTC long and short positions were liquidated.

Assessing whether leverage demand is predominantly toward buying requires an examination of Bitcoin’s futures monthly contracts. These contracts usually trade at a slight premium over the spot markets, as sellers ask for more money to postpone settlement. Typically, BTC futures should trade at an annualized premium of 5 to 10% — a condition known as contango, which is common across financial markets.

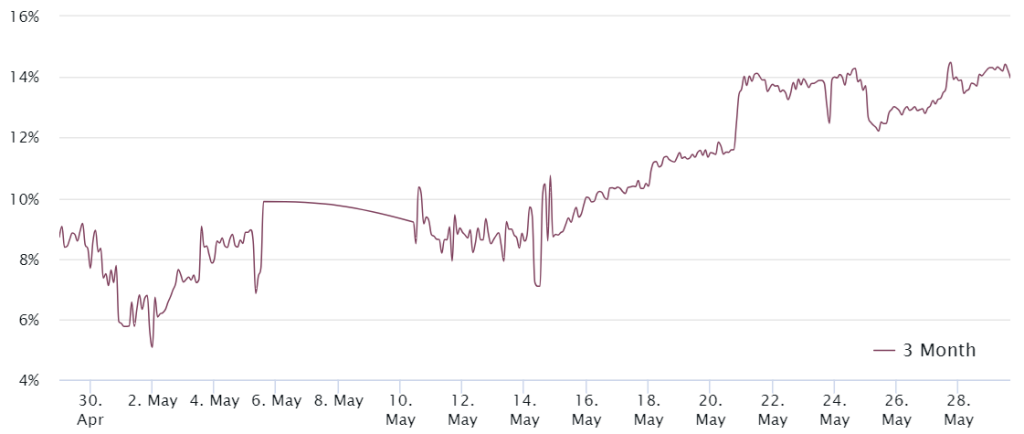

Recent data indicates a surge in demand for leveraged BTC long positions, with the premium breaking the 10% neutral mark four weeks ago. The premium recently peaked at 23%, the highest in over 18 months, with the current 21% level often reflecting excessive optimism. However, considering Bitcoin’s 40% price surge in the last two weeks, it’s too soon to consider the current futures premium as unsustainable, especially when past bull markets have seen premiums exceed 45%.

Retail trades buying above $72,000 could entice additional volatility

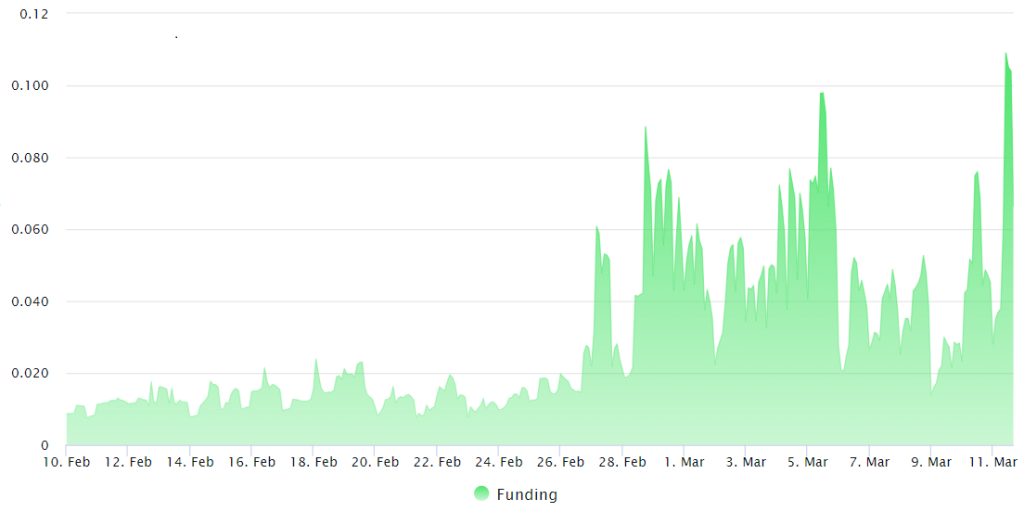

On March 11, the funding rate for Bitcoin futures perpetual contracts reached 2.1% per week, marking a peak unseen in over 18 months. Retail traders often prefer these contracts for their close tracking of the spot market prices, yet they come with a twist: a variable leverage fee, known as the funding rate. In essence, a positive rate suggests that traders are leaning more heavily on leverage for their long positions.

Related: Bitcoin breaches $71K for the first time

Bitcoin bulls have the advantage of strong inflows into spot exchange-traded funds (ETFs), and Microstrategy keeps on buying more Bitcoin, undeterred by the soaring prices. But, if retail traders jump on the bandwagon and start pouring into these pricey perpetual contracts at $72,000, there’s a good chance market makers and arbitrage desks will stir up some volatility to cash in on those over-leveraged positions.

While a few big players can’t really push Bitcoin’s price down for the long haul, the reality of investors paying a 2.1% fee every week to maintain bullish bets brings a real risk of a domino effect of liquidations if there’s a price dip. That said, with steady ETF inflows, it seems a bit off to predict a major price drop based just on the leverage scenario.

Responses