No Bitcoin ETF for Europe, but EU still leads in diversified crypto investments

The SEC has already approved several spot Bitcoin ETFs in the U.S.; however, these ETFs are not allowed in the EU due to strict regulations. Instead, there are other alternative ways to safely invest in cryptocurrencies.

After years of anticipation and over 20 rejected applications, the United States Securities and Exchange Commission finally approved a wave of spot Bitcoin (BTC) exchange-traded funds (ETFs) for trading on American stock exchanges.

These ETFs track the price of the world’s leading cryptocurrency one-to-one by directly purchasing and holding Bitcoin.

Previously, only Bitcoin futures ETFs were available in the United States. These track the performance of Bitcoin futures contracts, not the actual price of the cryptocurrency, and do not hold any real Bitcoin.

The newly approved spot ETFs offer both institutional and retail investors a regulated and convenient way to gain exposure to Bitcoin without the complexities of directly buying and storing it themselves. As regulated products, these ETFs are subject to SEC oversight and adhere to the same rules governing investment funds and codes of conduct for fund providers and managers.

But what does this approval say about the possibility of a Bitcoin ETF in Europe? Are financial regulators in the European Union ready to follow suit, or will EU investors have to wait longer?

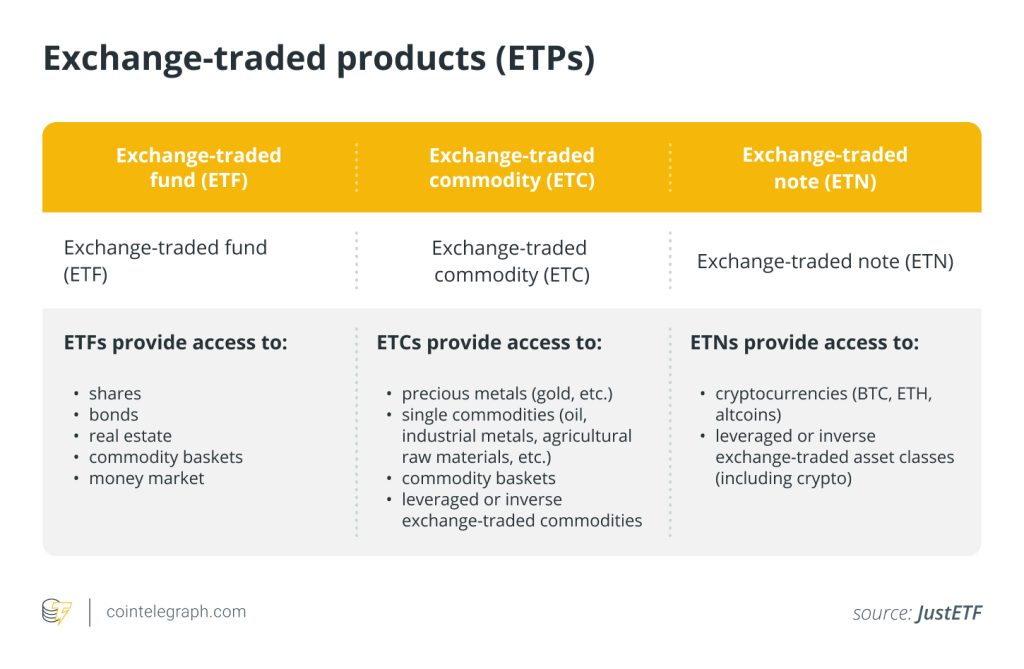

ETNs offer familiar route, but challenges remain

The European landscape for accessing Bitcoin and other cryptocurrencies remains relatively complex for investors. Retail trading and investment platforms such as Bison, Bitpanda and eToro offer convenient entry points, but their suitability for larger investors or those seeking traditional structures is limited.

Due to the Undertakings for Collective Investment in Transferable Securities (UCITS) regulation, if an ETF invests exclusively in Bitcoin — and thus in only one asset — it will not be approved in Europe.

One of the goals of this directive is to protect investors from total financial losses. These security measures also require that European fund products be diversified and not invest too heavily in a single asset class or product.

Therefore, if investors want to participate in the crypto market in EU countries, they have to rely on alternative products.

In Europe, these include, for example, Bitcoin exchange-traded notes (ETNs), which belong to the same category as ETFs, namely exchange-traded products (ETPs), and are often also backed by “physical” Bitcoin.

Several European investment companies, such as 21Shares, VanEck, ETC Group and Deutsche Digital Assets (DDA), offer such alternative investments in Bitcoin in the form of ETNs.

Dominik Poiger, chief product officer of Deutsche Digital Assets GmbH, told Cointelegraph that a clear advantage of ETNs is that they are easily tradable on exchanges such as Deutsche Börse’s Xetra, Euronext Amsterdam or SIX Swiss Exchange and that investors are already familiar with the concept of exchange-traded products.

“These products are then visible in the securities account as an allocation and can thus be easily used for portfolio diversification. The wrapper of the fully secured debt security is also well known to commodity investors — e.g., Xetra gold — so one is moving on the familiar territory,” he said.

Recent: Murder by (smart) contract: Ari Juels publishes crypto thriller

However, from a legal perspective, ETNs do not have the same legal protection as ETFs. In the event of an issuer’s insolvency, customer funds might not be separated from the bankruptcy estate, Poiger said.

Several providers have implemented multiple security measures to address this concern, including using regulated crypto custodians, independent security trustees and internal governance mechanisms.

According to Ophelia Snyder, co-founder and president of 21Share, the differences between ETFs and ETNs are hardly relevant if the product structure (spot price, physical collateralization) is appropriate.

For example, the potential default risk of the issuer of a 21Shares’ ETP is reduced by depositing the collateralized assets with an independent custodian. In this way, this investment vehicle also compensates for the claimed advantage of an ETF, which treats investor capital as a special fund and thus protects it from the issuer’s creditors in case of insolvency, Snyder explained.

As a financial instrument listed on regulated stock exchanges, European investors can easily buy and sell crypto-asset ETNs on the secondary market at the current market price on the exchange or over-the-counter, similar to their experience with shares or ETFs.

For institutional investors, some financial institutions can also offer special Alternative Investment Funds (AIFs). Such funds are not regulated at the EU level by the UCITS Directive.

They include hedge funds, private equity funds, real estate funds and a wide range of other institutional funds. AIFs can invest directly in cryptocurrencies, such as the HAIC Crypto Native Advanced Select from the German private bank Hauck Aufhäuser Lampe Privatbank AG.

However, this product is actively managed and only accessible to institutional investors — and is not an alternative for retail clients.

Will Bitcoin ETFs be approved in the EU in the future?

Poiger doesn’t see Bitcoin ETFs coming to Europe in this single-asset form like in the United States. The relevant directives in the EU state that crypto-assets, like gold or other commodities, are not UCITS-eligible assets, and “even if the EU were to change its rules and crypto assets were allowed to be bought directly in UCITS funds, they would still have to comply with the diversification rules of a UCITS.”

“So, it is very unlikely that there will ever be a pure Bitcoin UCITS ETF in Europe, but it is conceivable, albeit very unlikely, that a basket of cryptocurrencies would be approved as a UCITS fund.”

Simon Seiter, head of digital assets at Hauck Aufhäuser Lampe, told Cointelegraph that an ETF based on a crypto index with several cryptocurrencies would be possible. However, this would require the establishment of recognized crypto indexes that meet UCITS requirements. These could then serve as the basis for the ETF, similar to the way certain equity indexes are chosen as the basis for classic stock ETFs today.

“Under these circumstances, I see no need for regulatory change. In my view, whether UCITS funds should be opened up to single-asset ETFs goes beyond the crypto sector. If it becomes possible to issue crypto ETFs in compliance with UCITS requirements, I can definitely see a market for such products. This would allow retail clients to stay in their existing custody structures and still invest in cryptocurrencies in a diversified way,” he said.

Europe leads in diversified crypto investment options

Poiger believes that cryptocurrencies, especially Bitcoin, are emerging as a prominent asset class, as evidenced by the recent launch of a Bitcoin ETF in the United States.

“Crypto assets will become increasingly unavoidable for investors seeking diversification. We regularly analyze the impact of adding Bitcoin to a traditional portfolio (0.5%–2%) and have found that such an allocation has a positive impact on the risk-return profile, including volatility, Sharpe ratio and maximum drawdown, while improving performance.”

Recent: What the Bitcoin halving means for the network’s energy consumption concerns

In Europe, there are already many ways to invest in Bitcoin and crypto in general, Snyder said, so EU investors don’t need to despair about the absence of a Bitcoin ETF.

21Shares alone offers around 40 products in eight EU countries, including indexes, single asset products, liquid staking products and shorts, all fully backed by physical spot crypto assets.

These products are also listed on exchanges such as SIX and Xetra in multiple currencies. “Europe is well ahead of the U.S. in offering retail and institutional investors regulated access to crypto in an ETN/ETF wrapper,” said Snyder, adding that there is a high demand for cryptocurrencies in Europe as investors continue to see the value and opportunity in the asset class.

Responses