A beginner's guide to the different types of blockchain networks

Blockchain networks explained

Blockchain is a distributed, unchangeable ledger that makes recording transactions and managing assets (both tangible and intangible) in a corporate network much more accessible. On a blockchain network, virtually anything of value may be recorded and traded, lowering risk and cutting costs for all parties involved. But, what are blockchain networks?

A blockchain network is a technical infrastructure that allows applications to access ledger and smart contract services. Smart contracts are primarily used to originate transactions, which are then transmitted to each peer node in the network and recorded immutably on their copy of the ledger. End-users using client applications or blockchain network administrators are examples of app users.

Orders, accounts, payments, production and much more may be tracked using a blockchain network. You can see all facts of a transaction end to end since members share a single view of the truth, providing you with greater confidence and additional efficiencies and opportunities. So, how many blockchain networks are there?

Multiple organizations create a consortium to construct the network in most situations, and their permissions are governed by a set of policies that the consortium agrees to when the network is first configured. Other types of blockchain networks can be public, private, permissioned.

This guide will explain all the four types of blockchain networks, including their pros, cons and applications.

Key features of blockchain technology

Instead of a single authority, blockchain relies on a decentralized network of users to validate and record transactions. Blockchain transactions are consistent, fast, safe, affordable and tamper-proof because of this feature. These characteristics are explained below:

-

Fast: Transactions are delivered straight from the sender to the receiver, eliminating the need for one or more intermediaries.

-

Consistent: Blockchain networks operate around the world, 24 hours a day, seven days a week.

-

Inexpensive: Blockchain networks are less expensive to operate because they do not have centralized, rent-seeking intermediaries.

-

Secure: A blockchain's distributed network of nodes provides collective protection against attacks and outages.

-

Tamper-proof: Data is transparent and cannot be changed once it is time-stamped to the ledger, making the blockchain impenetrable to fraud and other criminal conduct. Similarly, everyone with access to a public blockchain network can see the transactions that have been created.

Types of blockchain networks

A blockchain network can be built in a variety of ways. They can be public, private, permissioned or constructed by a group of people called consortium.

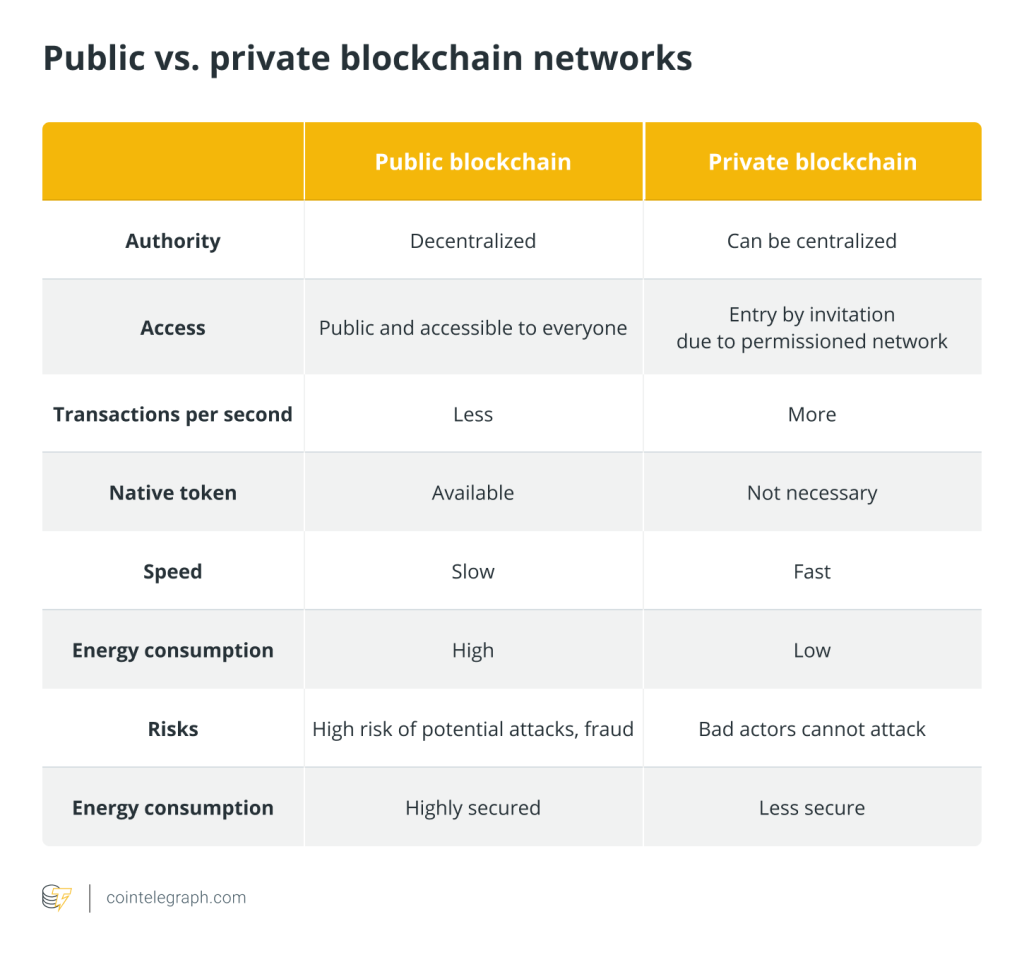

Public blockchain network

A public blockchain is one that everyone in the world may view, send transactions to, and expect those transactions to be included if they are valid and participate in the consensus process, which determines which blocks are added to the chain and what the current state is.

Cryptoeconomics — the combination of economic incentives with cryptographic verification using procedures such as proof-of-work (Bitcoin) or proof-of-stake (Ethereum) — secures public blockchains (Ethereum). These blockchains are regarded as “completely decentralized” in general.

Public blockchains offer a mechanism to safeguard app users from their developers by demonstrating that specific actions are beyond the scope of even the app's developers' authority. Because public blockchains are open, they are likely to be adopted by many organizations, with no need for third-party verification.

The anonymity of the public blockchain is another reason it has attracted so many supporters. Yes, it is a safe and secure open platform where you may conduct business properly and efficiently. Also, you are not required to divulge your true identity or name to participate. No one can trace your activity on the network if your identity is secured.

However, significant computing power is required, there is little or no privacy for transactions, and security is inadequate. These are crucial considerations for blockchain use cases in various industries.

Private blockchain network

Private blockchains, also known as managed blockchains, are permissioned blockchains that are administered by a single entity. The central authority in a private blockchain decides who can be a node.

In addition, the central authority does not always grant each node identical rights to execute functions. However, because public access to private blockchains is restricted, they are only partially decentralized.

Ripple (XRP), a business-to-business virtual currency exchange network, and Hyperledger, an umbrella project for open-source blockchain applications, are two examples of private blockchains.

For data confidentiality considerations, network sharing at the corporate level frequently necessitates a higher level of privacy. A private blockchain is the best option if this is one of your needs. Private blockchains are unquestionably a more stable network alternative because only a few users have access to particular transactions.

Moreover, in every industry, compliance is critical. Any technology that does not follow tight compliance rules is doomed to fail at some time. To make transactions seamless and straightforward, private blockchains follow and include all compliance regulations in their ecosystem.

Both private and public blockchains have disadvantages: Public blockchains take longer to validate new data than private blockchains, and private blockchains are more susceptible to fraud and bad actors. Also, the centralized approach frequently encourages an over-reliance on third-party management tools and favors the same few industry participants. Consortium blockchains were created to overcome these flaws.

Now that the fundamentals of public and private blockchain networks have been explained, let's sum up the differences between the two networks in the table below.

Consortium blockchain network

Consortium blockchains, unlike private blockchains, are permissioned blockchains administered by a consortium of organizations rather than a single institution. As a result, consortium blockchains have more decentralization than private blockchains, resulting in increased security.

On the other hand, setting up consortiums can be difficult because it necessitates collaboration between several businesses, which poses logistical issues and the risk of antitrust violations.

Furthermore, some supply chain members may lack the necessary technology or infrastructure to adopt blockchain technologies. Those who do may decide that the upfront costs of digitizing their data and connecting to other supply chain members are too high a price to pay.

The corporate software developer R3 has developed a popular set of consortium blockchain solutions for the financial services industry and beyond. CargoSmart has created the Global Shipping Business Network Collaboration, a non-profit blockchain consortium aimed at digitizing the shipping industry and allowing maritime industry operators to collaborate more effectively.

The consortium blockchain is supervised by one party, but it is protected against dominance. This supervisor can run their rules, make changes in balances, and terminate transactions that are proven to be full of faults as soon as each member agrees. Aside from that, it does various other tasks to provide result-oriented collaboration for businesses with the same aim.

Because the information from the checked blocks is hidden from public view, the consortium blockchain has a high level of privacy. Anyone who is a member of this blockchain, however, can access it. The consortium blockchain, unlike a public blockchain, has no transaction fees.

Another element of consortium blockchain that distinguishes it from public blockchain is its flexibility. Maximum validators may have issues with mutual agreement and synchronization in the public blockchain. Forks are formed as a result of such divergence, which does not occur in consortium networks.

Regardless of how many advantages consortium blockchain provides, it also has its drawbacks. One of the most significant drawbacks of this blockchain is that it is centralized, making it vulnerable to malevolent players. When the number of participants is restricted, it is assumed that one of them is to blame.

The launch of the consortium blockchain is a delicate process. All must approve the protocol for communication of the members. However, because an enterprise has less flexibility than a small business, establishing a public network connecting businesses is time-consuming.

Permissioned blockchain network

A permissioned blockchain network is typically set up by businesses that create a private blockchain. It's worth noting that public blockchain networks can be permissioned as well. This limits who is authorized to engage in the network and what transactions they can do. To participate, participants must first get an invitation or authorization.

Permissioned blockchain networks provide a decentralized platform, which implies that data is not stored in a central repository and that anybody can access it at any time and from any location. It ensures that all records have immutable signatures. The entire system is safe and data secure because all information exchange and transactions are encrypted cryptographically.

Furthermore, the network's miners and participants remain anonymous.

Another advantage of the permissioned blockchain is transparency. Everyone can see all of the data and information. However, this benefit has backfired, prompting concerns about data security in the permissionless blockchain.

One does not need to prove his or her identity on the permissioned blockchain. To join the network, all you have to do is dedicate your computing power. Any miner who determines the nonce value and solves the complex mathematical puzzle can join the system.

For many businesses, the permissionless blockchain system's limitations make it a risky proposition. They believe that using permissionless blockchain for selling enterprise solutions is not appropriate for them. Because of these drawbacks, Ethereum, a permissionless blockchain, is switching from proof-of-work to proof-of-stake as its consensus method.

Although anonymity is a good sign because the trading participants' identities remain hidden, it can also be troublesome. For example, in a scam or if someone tries to track down the persons involved in a transaction, the permissionless blockchain makes it impossible. As a result, many people are adopting blockchain for illegal activities because of these features.

Industries that benefit from various blockchain networks

Blockchain technology is beneficial in several areas, including supply chain, finance, real estate and gambling. Companies and individuals can avoid the cost and ambiguity of interacting with third parties to conduct regular business by using smart contracts, which are self-executing code stored and accessible on an immutable blockchain.

Bitcoin (BTC), Bitcoin Cash (BCH), Litecoin (LTC) and a slew of other payment-focused cryptocurrencies demonstrate the use of blockchain technology. Traditional third-party payment providers are in many ways less efficient and globally accessible than blockchain.

Furthermore, energy companies, such as gas and electric suppliers and utilities, can profit from blockchain in various ways. One such use is smart grids, which necessitate a local marketplace for power supply and demand. Another application of blockchain is to securely share data among smart meters in homes.

In addition, industries that rely on efficient and secure data ownership and management mechanisms, such as healthcare and digital identification, are discovering new cutting-edge solutions assisted largely by blockchain network protocols. Blockchains enable users to stay anonymous and secure data transfer using public-key cryptography, which provides users with a public key for receiving transactions and a private key for sending transactions.

For governments and agencies worldwide, blockchain may be a powerful tool for securing transactions, streamlining operations and fostering citizen trust. For example, governments can use blockchains to protect sensitive information such as birth dates, social security numbers, addresses and driver's license numbers. Another possible advantage of blockchain for the government is cost-cutting and inefficiency reduction. Blockchain technology can eliminate redundancies, streamline procedures and ensure data integrity.

Concerns surrounding blockchain technology

Despite the various advantages, blockchains that lack a stable ecology of network participants or a verified consensus process are vulnerable to attacks and centralized control. Decentralization and throughput — the amount of data a blockchain can process in a given amount of time — are important factors to consider. The Blockchain Trilemma — balancing and maximizing scalability, decentralization, and security in one network — is receiving much attention.

Other worries surrounding blockchain are related to the environment. The proof-of-work (PoW) consensus method, for example, often consumes a large amount of electricity to operate. Other concerns revolve around the technological complexity and intimidation factor that blockchain technology might bring to businesses and individuals.

The quick rise of cryptocurrencies on the global financial scene was only the beginning of blockchain technology's integration into business and our daily lives. More sectors are experimenting with blockchain technology, and more people are becoming aware of the utility and benefits that blockchain-based goods and services may provide in their everyday lives. Unfortunately, the blockchain business shows no signs of slowing down, and the technology has a lot of potential to become a component of, or maybe completely replace, our world's digital architecture in the future.

… [Trackback]

[…] Find More Information here to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Read More here on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Read More Information here to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Here you will find 80069 more Information to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] There you will find 73845 additional Info on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More Info here on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Read More Information here on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] There you will find 31152 more Info to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Information to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Info on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Info to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Here you can find 20403 more Information to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] There you will find 60899 additional Information on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Here you can find 90481 additional Info on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More Info here on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Here you will find 44706 more Information on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Read More Information here on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More on to that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Find More Information here on that Topic: x.superex.com/academys/beginner/3472/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/beginner/3472/ […]