Cryptocurrency losses and gains: Are they tax deductible or taxable?

Cryptocurrency tax rulings worldwide are mostly based on the 2014 ruling released by the United States Internal Revenue Service (IRS), which defines cryptocurrencies as capital assets. As such, cryptocurrencies are treated like stocks, bonds and other capital assets.

Considering crypto as a capital asset means crypto will be taxed whenever it is sold at a profit. Whenever you purchase something with cryptocurrency, your spending will incur a capital gains tax in the event that the amount you spent has increased in value compared to its original purchase price.

For example, let’s say a person purchases $100 worth of Bitcoin (BTC) and holds on to it until it rises to $1000 in value. Then, they spent the $1000 worth of BTC on gaming equipment. In this scenario, the $900 their initial $100 purchase earned would incur a capital gains tax — even if they spent the amount. Under the IRS ruling, the profit made from an initial purchase ($100) would still be taxable.

This is because, in the eyes of the IRS, most people treat crypto as an investment. As such, you owe crypto tax whether you spend or sell it—as long as your initial investment realizes a profit. If your crypto suffered a loss, you wouldn’t need to pay taxes upon selling or spending it.

Let’s circle back to our example earlier. To illustrate:

-

If your $100 purchase of Bitcoin was sold at $1000, your taxable gain is $900.

-

If your $100 purchase of Bitcoin was sold at $50, you would not owe any taxes. You could also use your $50 loss in Bitcoin to offset other investment gains.

How much taxes do you pay on crypto?

To be clear, the IRS classifies cryptocurrency as property and not currency. For this reason, the purchase and sale of cryptocurrency in the U.S. are both taxable. This means tax rules currently applicable to property are also applicable to crypto, except real estate tax rules.

In 2019, the IRS included a yes or no question for crypto transactions in tax return forms. As such, failure to report any income made from the sale of cryptocurrency is considered a violation of federal law and will merit a penalty.

The tax rates on cryptocurrency vary based on how much your crypto assets gain and the holding period for cryptocurrency. As such, when you report your earnings to the IRS, your income tax rate will be calculated relative to your current tax bracket. If your crypto earnings are high, this might also drive up your tax rate for other non-crypto earnings, as your tax bracket will likewise be adjusted.

How to calculate your cryptocurrency taxes

As mentioned, U.S.-based crypto holders are taxed based on two factors: their income and the holding period for their crypto. Let’s discuss the holding period for cryptocurrency.

The holding period for crypto technically begins when a person purchases cryptocurrency and ends when the crypto is disposed of as a capital asset via a sale, trade or other transaction.

Short-term capital gains

If your crypto has a holding period of 365 days or less, it will be subject to short-term capital gains tax. These gains are taxed just like your ordinary income and will depend on your current tax bracket.

For instance, short-term capital gains tax rates for 2022 are as follows:

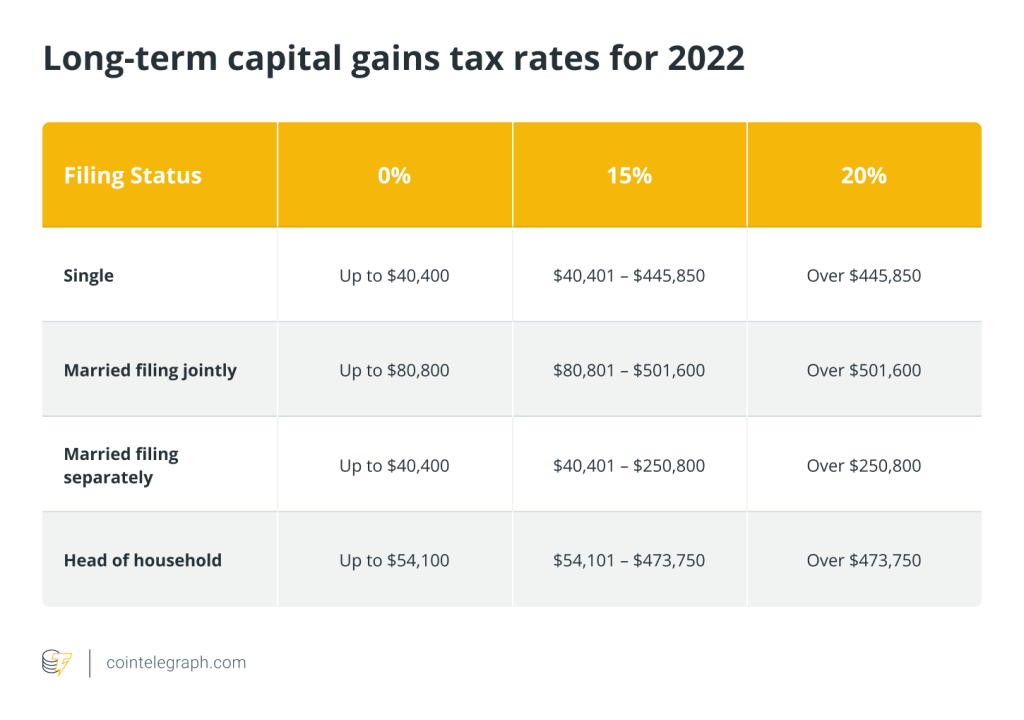

Long-term capital gains

On the other hand, cryptocurrency held for longer than 365 days will be subject to long-term capital gains tax rates. For instance, the tax rates for long-term capital gains in 2022 are:

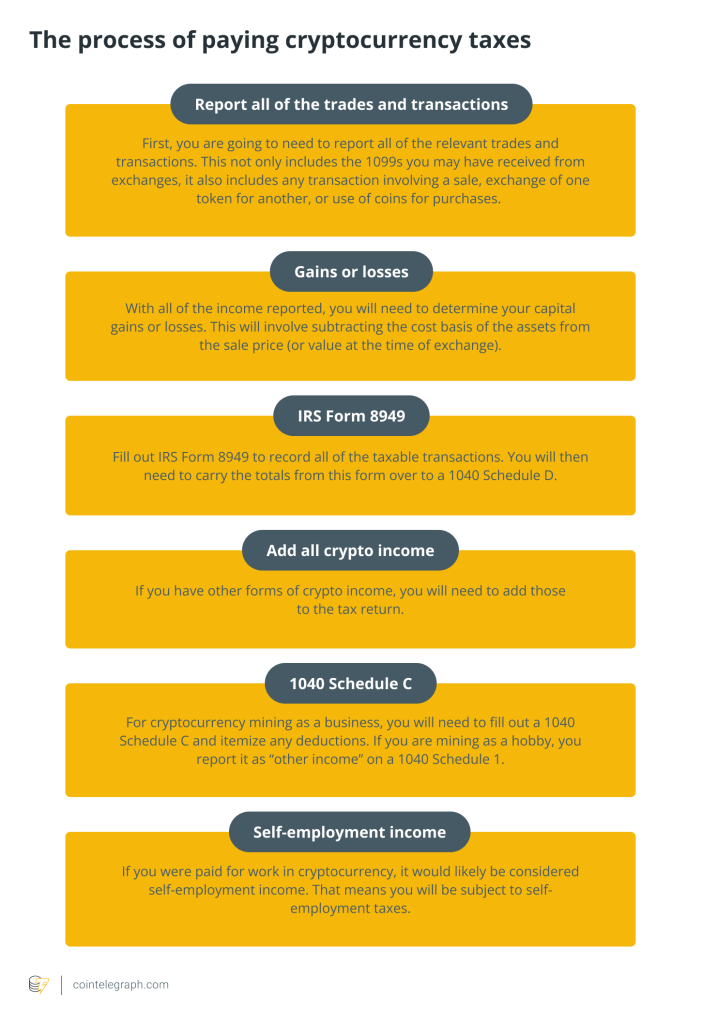

How to pay your cryptocurrency tax?

There are several platforms that US-based crypto holders can use to make filing and paying taxes on cryptocurrency much easier. Some popular tax reporting and payment options are Koinly, CryptoTaxCalculator, CoinLedger, Accointing and CoinTracker.

Taxes can also be reported and filed directly with the IRS through the use of the following forms:

-

Form 8949

-

Form 1040 tax return (Schedule D)

Some individuals with complex taxes (crypto or otherwise) consult with tax professionals. These include CPAs (certified public accountants), enrolled agents and tax lawyers.

Are cryptocurrency losses tax deductible?

As mentioned earlier, cryptocurrency losses can be used to reduce crypto taxes. Much like other capital losses, losses in crypto are tax deductible. This means you can use crypto losses to offset some of your capital gains taxes by reporting such losses on your tax return.

Up to $3,000 per year in capital losses can be claimed. Losses exceeding $3,000 can be carried over to future tax returns for deduction against future capital gains taxes. In addition, charitable donations using cryptocurrencies can also help reduce taxes.

Are cryptocurrency gains taxable?

Yes, crypto profits are treated much like gains on capital assets and are thus taxable. Remember that you are responsible for paying taxes on your crypto gains, even if you don’t receive any cash from the profits.

Because the IRS treats crypto assets like traditional capital assets (stocks and bonds), they are seen as property and are taxed as such. To compute your cryptocurrency gains tax, take your asset’s selling price and deduct the cost price. The resulting amount is your profit, which you might have incurred from trading or holding on to the asset for a time. Your crypto tax liability will then be computed based on the rates and holding periods discussed earlier.

Do you need to report crypto if you didn’t sell it?

Purchasing cryptocurrency is not a taxable event. This means if you’re only holding on to your cryptocurrency, you are not required by law to report and pay taxes. Owning cryptocurrency does not immediately incur gain or loss, so it is not taxed—even if it is appreciating in value.

So, how about moving your crypto between wallets or from one exchange to another?

These types of transfers are also not taxable. You do not need to report or pay taxes on them. However, if you receive crypto as income, for example, in the form of a salary or rewards from a blockchain project, that is considered taxable. You will need to calculate the fair market value of the cryptocurrency at the time you received it and pay taxes on the resulting amount.

Receiving crypto gifts is a non-taxable event for both the giver and the receiver, as long as the value of the gift is below the annual gift tax exclusion limit ($15,000). The same goes for the inheritance of cryptocurrency.

Does the IRS know if you own cryptocurrency?

The short answer is: maybe. The IRS has been increasing its efforts to track down cryptocurrency owners who have not been paying their taxes. In 2019, the IRS launched a task force focused on crypto compliance and sent letters to over 10,000 U.S. taxpayers who may have failed to report their crypto holdings and gains.

Currently, however, taxpayers are asked to declare their crypto activities on Form 1040. These activities include receiving, selling, sending, exchanging or acquiring an interest in cryptocurrency. As such, the non-declaration of crypto activities may increase the chances of an IRS audit.

How do DeFi and NFT taxes work?

So far, current IRS rulings on cryptocurrency tax do not specifically mention decentralized finance (DeFi). However, DeFi and yield farming transactions may still be considered taxable under the general crypto asset tax rules, as they involve cryptocurrencies.

The same goes for taxes on nonfungible tokens (NFTs). While the IRS has not released any guidance on how to tax NFTs, they are most likely taxable as property under current IRS rules. This means if you sell an NFT, you will have realized a profit and are thus required to report it as a capital gain.

Can you avoid crypto tax?

There are various ways to avoid paying taxes on your crypto profits, such as giving away crypto as charity or gifting it to friends and family. These methods are perfectly legal and can help you reduce your tax liability.

Platforms such as the Giving Block facilitate crypto donations to nonprofits and emergency funds, such as Mental Health America, Children’s Cancer Association, Ukraine Emergency Response Fund and more. Donors can also choose to donate crypto to causes such as education, crypto adoption, animals or women empowerment.

That said, the best option to avoid IRS audits and penalties is to declare crypto-related activities and pay crypto taxes on time. This way, crypto holders can avoid any inconvenience that non-filing or non-payment may cause.

Purchase a licence for this article. Powered by SharpShark.

… [Trackback]

[…] Find More Information here to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More Information here to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Read More on on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Read More Information here to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Info on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] There you can find 28419 additional Information on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Here you will find 87511 more Info on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More Info here to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Here you can find 45879 more Info on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Info on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More Information here on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More here on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] There you will find 34798 additional Info to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More here to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Read More here on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More here on that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/beginner/2401/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/beginner/2401/ […]