Post-Shanghai ETH Upgrade: Things We Must Know

Summary

Ethereum will complete the Shanghai Upgrade in April, staking and withdrawing option will be enabled on Beacon Chain. The Shanghai Upgrade is a hard fork of the Ethereum execution layer, which is expected to fulfill 9 EIPs. As of March 14, 2023, approximately 17.5M ETH have been in staking, accounting for 15.25% of the total ETH supply. Validators on Ethereum has accumulated more than 2 ETH as staking rewards on average, and more than 1 million ETH will be released to the market after the Shanghai upgrade. The impact of the Shanghai upgrade on the Ethereum ecology is undoubtedly significant. This report will mainly discuss the withdrawal design and related risks of Ethereum and LSD protocols after the Shanghai Upgrade, as well as the impact on the price of ETH and other tokens related to the LSD protocol.

Chapter 1 — Official withdrawal process of Ethereum

Withdrawal is achieved by the simultaneous upgrade of the execution layer and consensus layer, and two options are available: "Partial Withdrawal" and "Full Withdrawal". Partial Withdrawal is to withdraw only the part of proceeds, whereas Full Withdrawal is to withdraw from the validator node and withdraw all the proceeds plus that in staking. There is no priority between these two types of withdrawals, which will be executed automatically as long as the necessary conditions are met.

(1)Necessary condition: Validator must have 0x01 Credential (also known as proof of deposit for active validators, currently 42% of validators have this proof)

(2)Partial withdrawal conditions: Validator is active and the balance is greater than 32ETH

(3)Full withdrawal conditions: Validator is in the Withdrawable state (this usually means the Validator already quitted the network)

The number of withdrawal requests executed by the Ethereum Beacon Chain in a fixed period of time is strictly limited, and each block can process a maximum of 16 withdrawal requests. After a validator meets the withdrawal conditions and makes a request, a withdrawal list is created to contain all validators who submitted withdrawal requests, which includes the withdrawal order, receipt address on execution layer and withdrawal amount. Withdrawal requests are all initiated on the consensus layer and do not proceed independently or enter the memory pool of transactions, and the withdrawals are exempt from the gas, nor do they increase the gas.

Chapter 2 — Will there be a selling climax of ETH?

According to Beaconcha.in, as of March 14, 17,573,625 ETH have been in staking on the Beacon Chain. The number of active validators is 549,181, and staking per validator is currently 33.98 ETH on average at a total of 18,661,170.4 ETH on the Beacon Chain.

Based on the withdrawal conditions and process, there are 512 validators per Epoch to withdraw (32 slots per Epoch, one block per slot) and 115,200 validators will participate in the withdrawal in a day (12 seconds per block, 7,200 blocks per day); the total withdrawal capacity is 3,686,400 ETH per day, ceteris paribus, it takes about 5.06 days to withdraw all the ETH in staking on the chain, based on the current number of ETH in staking. However, the process of executing the withdrawals demands some time, and all exiting validators need to wait at least 27.3 hours before they can start a withdrawal.

ETH staking started in November 2020 when the price of ETH is between $500-$600, and these long-term staking would be eager to pull out the principal and the rewards. Stakings starting from February 2021, on the other hand, are losing money relative to the current price. Most withdrawal requests will be Partial Withdrawal. Therefore, a selling climax is not inclined to appear as the selling will be mostly early stakers, which is still minority.

The withdrawal process is not always smooth, for some withdrawals are invalid if the withdrawal conditions are not met, especially in the case that the proof of deposit, 0x00 Credential, is to be converted to 0x01 Credential after the Shanghai upgrade. this conversion is also limited to 16 requests per block. 0x00 Credential validators are on average older with more staking rewards, which leads to a gradual increase in the total amount of ETH withdrawn per block. In the extreme case, exodus from validator nodes is not likely to occur, and each staking protocol is enforced by the Churn Limit Quotient, which reduces the selling pressure to some extent. From the above analysis, the selling pressure is likely to peak 3 to 4 days after the Shanghai upgrade.

In addition, according to data from Glassnode, the total number of nodes willing to relieve from the validator role is about 920. Meanwhile, due to regulatory reasons, the majority of ETH tokens in staking through centralized institutions, which may include Kraken (6.52%) and Binance (4.92%) that have over 2 million ETH in staking, will be released; and in extreme cases, it will be cleared. It will take a month for all withdrawals to be completed according to the Churn Limit Quotient of validators. However, these ETH will not be fully circulated in the market and instead end up in staking on other protocols.

Chapter 3 — Status and withdrawal design of various LSD protocols

3.1 Performance of Liquidity Staking Token (LST)

Currently, the total ETH staking volume of all types of LSD protocols accounts for 42.97% of all staking volume, and Lido alone has accounted for over 30%. The tokens derived from these protocols for staking, LST, have been circulating in the secondary market prior to the Shanghai upgrade with considerable yield in DeFi.

LST tokens have accounted for about 65% of the staking volume; these staking tokens, on the other hand, have seen significant discounts over the past two years. Currently, the overall liquidity of LST is positive due to the approaching Shanghai upgrade. The opening of withdrawals is favorable for LST price, but it also tests the risk management ability and withdrawal process design of each LSD project.

stETH is currently the LSD token with the best liquidity. As demonstrated by the stETH/ETH price curve in the chart below, the price of stETH/ETH saw a massive discount during March 2021 and June 2022, corresponding to the 3AC and FTX incident, respectively, which are triggered by the immobility of liquidity. The sell-off in 2021 coincided with the climax of the market, which are mostly users staking at the end of 2020; they exited at a higher profit.

Coinbase's LST token, cbETH, has previously been in a discounted state. cbETH is mainly in Uniswap, and it currently reached an approximate TVL of $7.5M; low daily trading volume is encountered, and a liquidity crisis may occur. However, the performance has been outstanding recently. It is possible that as the Shanghai upgrade approaches, arbitrageurs could profit by buying cbETH at a discounted price.

Rocket pool holds the third largest market share among the LSD protocols, with a market cap of $391M and a circulation supply of 210K for its derivative token, rETH. After the Shanghai upgrade, rETH can be returned to the protocol and redeem the ETH in staking as well as the corresponding rewards, in this case, rETH has been priced higher than ETH in the secondary market.

3.2 Comparison of the withdrawal process of each LSD protocol

The design of withdrawal scheme of each LSD protocol is subject to uncertainty, and the Shanghai upgrade of Ethereum is a refinement of the PoS mechanism yet a challenge to the LSD protocol as the protocol needs to balance between user experience, processing speed and security. The overall PoS withdrawal process on Ethereum is complicated, especially the different time allocation on various withdrawal protocols. After the Shanghai upgrade, various LSD protocols may be exposed to attacks due to flaws in design. Most of the withdrawal designs will address the following two aspects:

(1) Avoidance of attacks and arbitrage: the exchange of LST tokens for ETH may have room for arbitrage activities, reducing the protocol APR; ensure there are sufficient amount of ETH for users to redeem, etc.

(2) Setting of thresholds for withdrawal and improve user experience at the same time, especially on waiting time.

3.2.1 Lido

Lido v2 has been approved by the community. The withdraw design has two modes: Turbo and Bunker. Lido creates a withdrawal buffer for withdrawals, which is mainly composed of 3 parts: execution level rewards, ETH as withdrawal and ETH in staking. After the Shanghai upgrade, Lido will have 200k ETH available for immediate withdrawal (without going through the exit of validator node process), and this amount can be the initial buffer.

(1)Turbo mode: Once there is sufficient ETH, the protocol will fulfill the withdrawal request. The request time varies from 1 hour-3/4 days; the waiting time depends on whether there is sufficient ETH as the buffer (requires exit of the validator node).

(2)Bunker mode: This mode is triggered if there is a widespread forfeiture of the Lido validator nodes; once the mode is activated, the losses will be distributed to users when the forfeited validator nodes exit and the losses can be estimated. Meanwhile, the stETH:ETH redemption calculation must perform accurately. Withdrawals under this mode may take more than 36 days.

Once a user's withdrawal request enters the queue, an NFT will be given, which represents the position in the queue. This NFT can be traded in the secondary market, where bidders could buy a position in the front of the queue. If the price of ETH is volatile in April, there will be plenty room for imagination on secondary market. Once there is a forfeit during the request period, users in the queue also have to bear the burden to share the penalty equally. However, there is no reward for stETH withdrawal requests in the queue in order to avoid malicious arbitrage attacks.

In addition to the above design, in order to avoid attacks and arbitrage activities, Lido mandates more terms on withdrawals, such as withdrawal requests cannot be cancelled, and the redemption rate of the request cannot precede the redemption rate at the time the request was created.

3.2.2 Rocket pool

Rocket Pool introduces minipools, which reduces the capital requirements for validators, requiring only 17.6 ETH to operate as a minipool; and when the pool is withdrawn, the validator's capital will be the first to experience losses so that the rETH holders are endowed with insurance at 110%.

For withdrawal requirements, a deposit pool is in place that rETH redemptions can be achieved from the deposit pool and partial withdrawals; but once drained, rETH can be converted to ETH at discount on the secondary market, which is an arbitrage opportunity for minipool operators as rETH can be purchased from the secondary market at a discounted price, and Rocket Pool's burning mechanism will help exit minipools, thus guaranteeing an exchange rate of rETH:ETH=1:1. Therefore, the operator of minipools can choose whether to exit or withdraw the reward, which is entirely determined by market behavior.

For Rocket Pool, the withdrawal process is not complicated: the operator only needs to revoke minipools; what’s more important, the liquidity of the protocol's deposit pool must be ensured so that rETH can be redeemed smoothly. At the time of the Merge of Ethereum, Rocket Pool handled it well while one of the node operators of Lido experienced severe downtime. Evidently, Rocket pool will perform better in dealing with the withdrawal process during the Shanghai upgrade. The Atlas upgrade launched by Rocket Pool will lower the threshold to become a validator, further driving rETH liquidity and RPL price.

3.2.3 Frax Finance

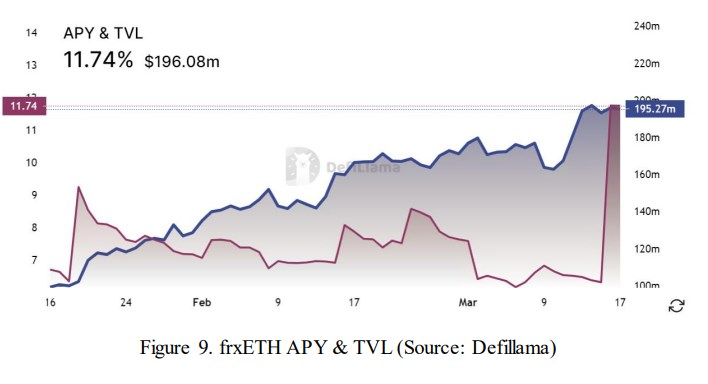

frxETH does not accumulate staking rewards when users staking ETH via Frax; instead, ETH can be redeemed within the protocol. In order to receive the staking rewards, users need to re-deposit frxETH into the protocol and exchange for sfrxETH. As a result, Shanghai upgrade will not have influence on redemption within Frax; it is more critical to consider whether the protocol could provide enough ETH for redemptions. Especially when Frax can no longer attract users by higher returns, there may be a large number of redemptions.

3.2.4 StakeWise

StakeWise offers a liquidity staking service similar to Lido, except that StakeWise has a new v3 to mitigate the risk of centralized validators; but this version is not yet available. There are two mechanisms of staking on StakeWise: Pool and Solo. The Pool mechanism is a staking pool for any ETH holder to participate, and the Solo mechanism is a non-custodial staking service for each user with 32 ETH.

In terms of exit, users under the Pool mechanism cannot destroy sETH2 and rETH2 within the protocol and receive ETH 1:1 until the completion of the Shanghai upgrade. Prior to the Shanghai upgrade, there was a secondary market for sETH2 and rETH2. Solo users could choose to voluntarily exit before the Shanghai upgrade, but the balance was inaccessible and not eligible to re-enter the staking; by choosing to voluntarily exit after the Shanghai upgrade, fees would continue to accrue until fully exited, which could take a few days.

Chapter 4 — Conclusion and thoughts

The Shanghai upgrade will exert an impact on the LSD protocol in three aspects: (1) token prices, including ETH, various LSD protocol tokens, and derivative token prices; (2) withdrawal design tests the technology of each LSD protocol, and users may choose a different protocol; and (3) more DeFi protocols based on Ethereum staking or LSD protocol derivatives will emerge.

Once users are able to re-select staking protocols, the competitive landscape of Ethereum staking will be reshuffled. Moreover, new LSD protocols or staking-based mechanisms will be introduced, such as DVT-based applications and EigenLayer's re-staking concept, which may have better yields. For most ETH staking users, the initially decided staking method and object can be changed after the Shanghai upgrade, and the market share of ETH staking will be redetermined.

Users will pay attention on more liquidity staking protocols in terms of smoothness of withdrawal design, staking revenue, license-free, and security. Other than Lido, Rocket Pool may be the LSD protocol with the best growth; the number of minipools and the token price are recommended to be traced after the Shanghai upgrade, especially the withdrawal design, reward mechanism and scalability are addressed in the Atlas upgrade.

LSD-based index tokens have already emerged. For example, gtcETH is jointly launched by Gitcoin and Index Coop, a new Ethereum staking index token. It aims to provide a proxy that users could receive mixed earnings from multiple liquidity staking protocols. At the same time, it facilitates the growth of multiple LSD so that Ethereum can be further distributed. In addition, more DeFi applications will be created: (1) LST can be deemed as the original pool for minting new derivatives; (2) the emergence of futures products anchored to the yield or inflation rate of ETH; and (3) the emergence of stablecoin based on staking ETH. The release of Ethereum staking may also create incremental volume to lending protocols, and many articles have dissected the possibility of high returns because of re-staking.

References:

1. https://github.com/ethereum/consensus-specs/blob/dev/specs/capella/beacon-chain.md#has_eth1_withdrawal_credential

2. https://tim.mirror.xyz/zLdl8bEiDmobHZ5RlvG2LrlZLWV9c2XvkuKQ-vpljSU

3. https://coinvoice.cn/articles/29918

4. Gitcoin Launches gtcETH Index Token To Bolster Funding – The Defiant

5. https://hackmd.io/@lido/SyaJQsZoj

6. Partial withdrawals after the Shanghai fork

https://dataalways.substack.com/p/partial-withdrawals-after-the-shanghai

About Huobi Research Institute

Huobi Blockchain Application Research Institute (referred to as “Huobi Research Institute”) was established in April 2016. Since March 2018, it has been committed to comprehensively expanding the research and exploration of various fields of blockchain. As the research object, the research goal is to accelerate the research and development of blockchain technology, promote the application of the blockchain industry, and promote the ecological optimization of the blockchain industry. The main research content includes industry trends, technology paths, application innovations in the blockchain field, Model exploration, etc. Based on the principles of public welfare, rigor and innovation, Huobi Research Institute will carry out extensive and in-depth cooperation with governments, enterprises, universities and other institutions through various forms to build a research platform covering the complete industrial chain of the blockchain. Industry professionals provide a solid theoretical basis and trend judgments to promote the healthy and sustainable development of the entire blockchain industry.

Contact us:

Website:http://research.huobi.com

Email:[email protected]

Twitter:https://twitter.com/Huobi_Research

Telegram:https://t.me/HuobiResearchOfficial

Medium:https://medium.com/huobi-research

Disclaimer

1. The author of this report and his organization do not have any relationship that affects the objectivity, independence, and fairness of the report with other third parties involved in this report.

2. The information and data cited in this report are from compliance channels. The Sources of the information and data are considered reliable by the author, and necessary verifications have been made for their authenticity, accuracy and completeness, but the author makes no guarantee for their authenticity, accuracy or completeness.

3. The content of the report is for reference only, and the facts and opinions in the report do not constitute business, investment and other related recommendations. The author does not assume any responsibility for the losses caused by the use of the contents of this report, unless clearly stipulated by laws and regulations. Readers should not only make business and investment decisions based on this report, nor should they lose their ability to make independent judgments based on this report.

4. The information, opinions and inferences contained in this report only reflect the judgments of the researchers on the date of finalizing this report. In the future, based on industry changes and data and information updates, there is the possibility of updates of opinions and judgments.

5. The copyright of this report is only owned by Huobi Blockchain Research Institute. If you need to quote the content of this report, please indicate the Source. If you need a large amount of references, please inform in advance (see “About Huobi Blockchain Research Institute” for contact information) and use it within the allowed scope. Under no circumstances shall this report be quoted, deleted or modified contrary to the original intent.

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More Info here on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Here you can find 54341 additional Information on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More on to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Here you will find 28956 additional Information on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More Information here on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Information to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Find More Information here on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Info on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More here on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Find More here to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More Information here to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Find More on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Information on that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Here you will find 99846 additional Info to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Read More Information here to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Find More on to that Topic: x.superex.com/academys/deeplearning/2038/ […]

… [Trackback]

[…] Find More to that Topic: x.superex.com/academys/deeplearning/2038/ […]