Lido launches institutional-grade liquidity staking solution

The biggest ETH liquid staking protocol has enhanced its offering for large investors, many of whom are already its customers.

Lido Finance has introduced Lido Institutional, an institutional-grade liquidity staking solution aimed at large customers such as custodians, asset managers and exchanges.

Lido Institutional is a middleware solution that “combines the reliability and security necessary for enterprise-grade staking with the liquidity and utility required for diverse institutional strategies,” Lido said in a post on X.

Lido Institutional already has a customer base

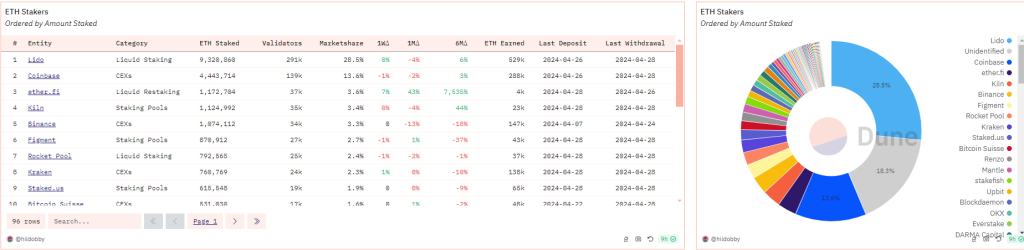

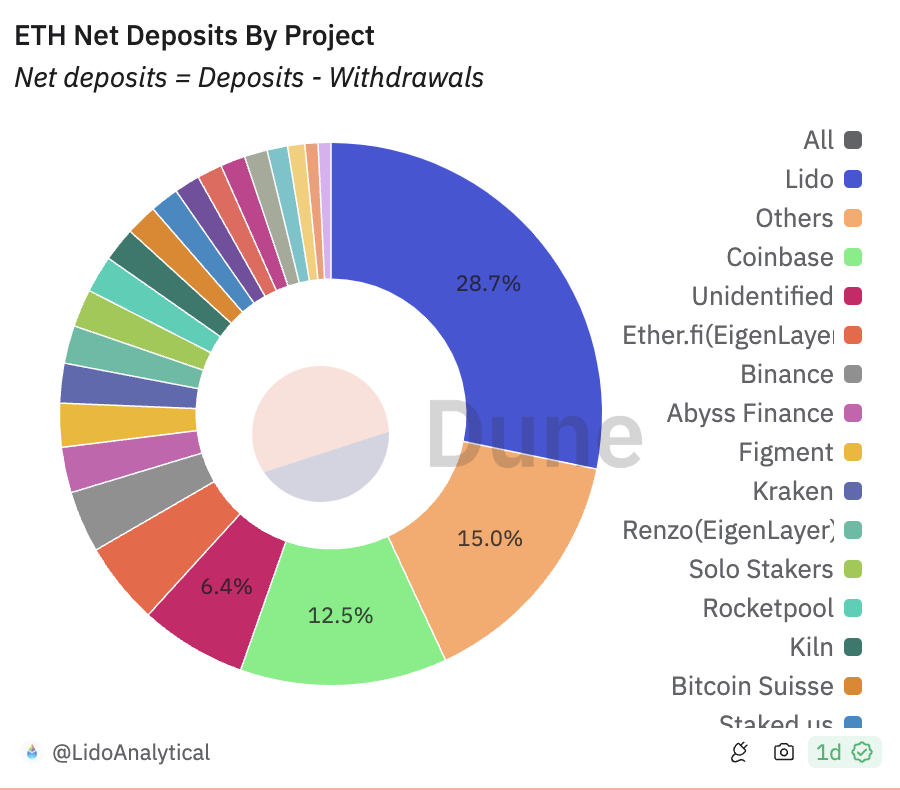

Lido is the largest liquid staking protocol, controlling over 28.5% of all staked Ether (ETH). That share was down from 32% in December, but it already represents a large institutional customer base, as the decentralized autonomous organization (DAO) noted in its announcement:

“Lido already stands out as a premier choice for many institutions looking to engage in Ethereum staking.”

Lido has been working up to the launch of the new service. It teamed up with infrastructure provider Taurus in February. Lido and infrastructure provider Fireblocks announced their integration at the EthCC event in July. Lido Institutional designates those firms as custody solutions on its website.

Related: Lido, Rocket Pool team members argue over decentralization

Launched in 2020, Lido is a liquid staking solution governed by the Lido DAO. It allows users to stake any amount of ETH as part of a pool and receive rewards for it, rather than coming up with a minimum of 32 ETH to stake directly on the network. At the same time, users can use their Lido Staked ETH (STETH) for other activities. Lido takes a 10% fee on staking rewards, which is split between node operators and the DAO treasury.

Staking faces US regulatory threat

The United States Securities and Exchange Commission claimed that Lido and its competitor Rocket Pool sell unregistered securities in the complaint it filed against Consensys in June. According to the SEC:

“Investors make an investment of ETH in a common enterprise with a reasonable expectation of profits from the managerial efforts of Lido and Rocket Pool, respectively.”

“Yet, neither Lido nor Rocket Pool has filed a registration statement with the Commission for the offer and sale of these investment contracts,” the complaint continued.

The SEC claimed that Consensys’ MetaMask platform acted as an intermediary in unregistered securities transactions by facilitating transactions through Lido and Rocket Pool. The SEC has not taken direct action against Lido or Rocket Pool, but its position is clear.

Magazine: Are DAOs overhyped and unworkable? Lessons from the front lines

Responses